How Much Are Nursing Home Fees in the UK? (2026 Costs)

Understanding the cost of nursing home care is a significant challenge for many families. The question of how much are nursing home fees uk is often the first and most critical one, but the answer can be complex. High figures, a confusing funding system, and unclear additional charges can make planning feel overwhelming, creating uncertainty about affordability and the future of family assets like the home.

At Guide2Care, we aim to provide the clear, practical, and up-to-date information you need for 2026. This guide breaks down the average nursing home costs across England, Scotland, Wales, and Northern Ireland, reflecting the latest available data. You will learn what factors influence the final price, what is typically included in your fees, and how to identify potential extra costs. We also explain the different funding routes, from local council support to NHS Continuing Healthcare, so you can understand who is responsible for payment and create a realistic budget with confidence.

Key Takeaways

- Understand the average weekly cost for nursing care and see how it differs from standard residential care fees across the UK.

- Discover the key factors that determine how much are nursing home fees uk, from the home's location to the level of care required.

- Determine if you will need to self-fund care or if you are eligible for financial support from your Local Authority or the NHS.

- Follow a clear, 4-step plan to manage the process, from getting a care needs assessment to finding the right home.

Understanding Average Nursing Home Costs in the UK

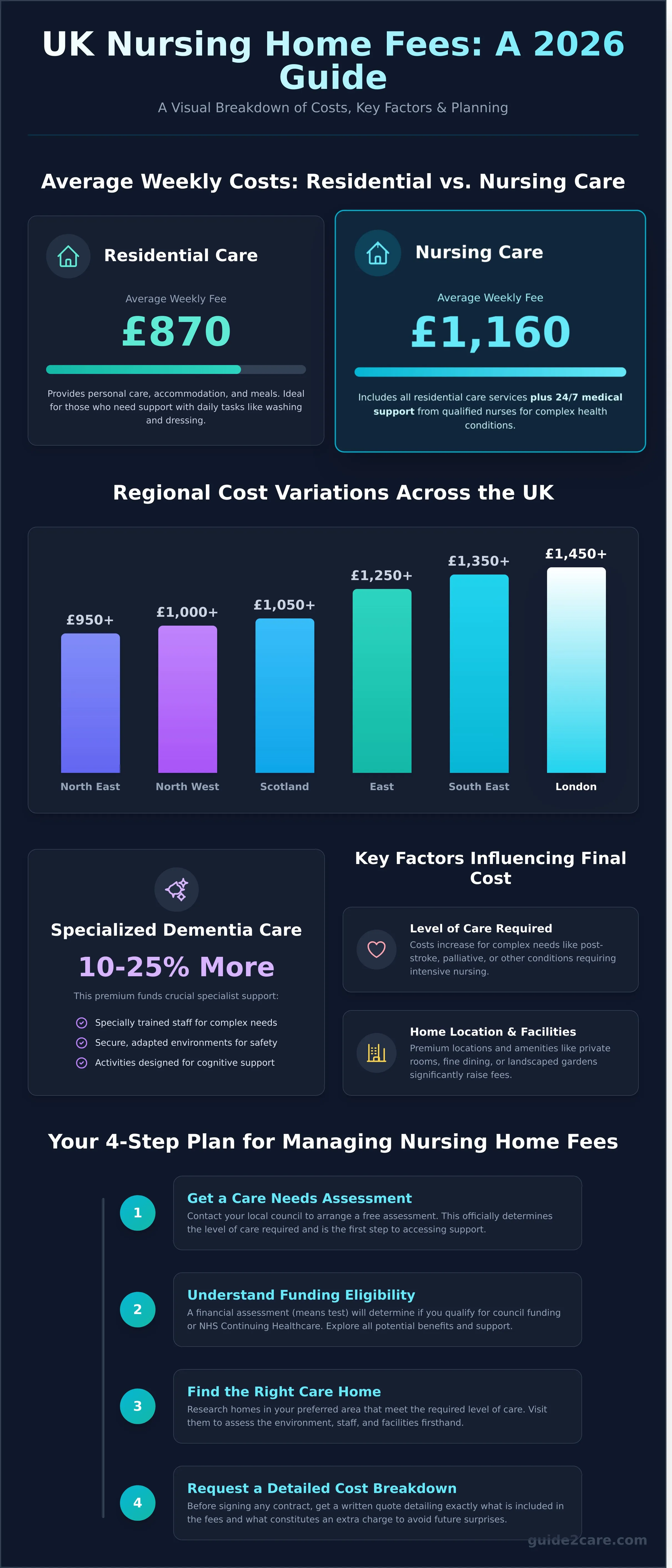

When asking how much are nursing home fees uk, it is important to understand the national averages while recognising that prices vary significantly. As a starting point, the average weekly fee for a residential care home is around £870, while a nursing home costs approximately £1,160 per week. These fees cover the comprehensive cost of 24/7 personal care, specialist medical support, accommodation, and meals. The structure of Nursing home care in the United Kingdom means these costs are often means-tested, a topic we cover later in this guide.

To better understand the factors that influence these fees, watch this helpful video:

Average Weekly Fees: A Snapshot (Residential vs. Nursing)

A nursing home is more expensive than a residential home for one key reason: the provision of 24-hour medical care by qualified nurses. While residential homes provide personal care and support with tasks like washing and dressing, nursing homes are equipped to manage more complex health conditions, administer medication, and provide intensive medical treatment. This on-site nursing expertise is the primary driver of the higher cost.

Regional Cost Variations Across the UK

Location is the most significant factor affecting care home fees. Costs are highest in London and the South East, reflecting higher property values and staff wages. The North of England, Scotland, and Northern Ireland typically offer more affordable options. Always research costs in your specific town or city for an accurate estimate.

| Region | Estimated Weekly Nursing Home Fee |

|---|---|

| South East England | £1,350+ |

| London | £1,450+ |

| East of England | £1,250+ |

| North West England | £1,000+ |

| North East England | £950+ |

| Scotland | £1,050+ |

Dementia Care: Understanding the Additional Costs

Care for individuals with dementia often requires a higher fee, typically 10-25% more than standard nursing care. This premium covers the cost of specially trained staff who can manage complex behaviours and communication needs. It also funds secure, adapted environments that ensure resident safety and specialised activities designed to support cognitive function and well-being.

What Factors Influence the Final Cost of a Nursing Home?

The average figures provide a useful benchmark, but understanding how much are nursing home fees uk for a specific individual requires a closer look at key variables. The final price you are quoted is determined by a combination of personal needs, the home's location, and the services you choose. Before committing, it is essential to get a detailed breakdown of all costs in writing.

The Level of Care and Individual Needs

The most significant cost factor is the complexity of care required. A resident needing basic personal support will have lower fees than someone with significant medical needs. Costs increase for conditions requiring specialist attention from registered nurses, such as advanced dementia, post-stroke care, or palliative care. If a resident's primary need is for nursing, they may be eligible for a non-means-tested payment from the health service called NHS-funded nursing care, which is paid directly to the home.

The Care Home's Location and Facilities

The location and quality of the home play a major role in determining fees. A home in Central London or Surrey will cost significantly more than one in a less expensive region. Homes with premium facilities like private cinemas, landscaped gardens, or fine dining restaurants carry higher price tags. Similarly, a care home with an 'Outstanding' CQC rating often charges more due to high demand and proven quality. The type of room also affects the price, with larger rooms, en-suite facilities, and better views costing more.

Included as Standard vs. Potential Extra Charges

To understand the true cost, you must clarify what is included in the standard weekly fee and what is charged as an extra. Never assume everything is covered. Always ask for a complete list of additional charges before signing a contract.

- Fully furnished accommodation

- Utility bills (heating, lighting, water)

- All meals, drinks, and snacks

- The core, personalised care plan

- Basic laundry services

- Access to communal lounges and gardens

What Often Costs Extra?

- Hairdressing and salon treatments

- Chiropody or physiotherapy

- Newspapers and magazines

- Personal toiletries

- Private phone line and internet access

- Escorted trips and social outings

- Alcoholic drinks

Who Pays for Care? Self-Funding vs. State Support

Once you have an estimate of how much are nursing home fees UK, the next critical question is who is responsible for payment. In the UK, funding for care follows one of two routes: you either pay for it yourself (known as 'self-funding') or you receive financial support from your local authority. The path you take is determined by a formal financial assessment.

The Financial Assessment (Means Test) Explained

Your local council conducts a financial assessment, or 'means test', to decide if you qualify for state support. This is a detailed evaluation of your income, savings, and assets (capital). It calculates how much, if anything, you must contribute towards your care fees. The assessment includes weekly income like pensions and benefits, plus capital such as bank savings, investments, and property. Importantly, the value of your main home is usually included when assessing for a permanent move into a care home, but not for care provided in your own home.

Capital Limits in England, Scotland, Wales, and Northern Ireland

The means test uses set capital limits which vary across the UK. For 2024/2025 in England, the thresholds are:

- Upper Capital Limit: £23,250

- Lower Capital Limit: £14,250

Your eligibility for council funding depends on where your capital falls:

- Above £23,250: You will be expected to pay for your care in full. You are a 'self-funder'.

- Between £14,250 and £23,250: You will receive some council funding, but you must contribute from your income plus a 'tariff income' from your capital. This is calculated as £1 per week for every £250 you have between the two limits.

- Below £14,250: You will receive maximum support from the council. You will still contribute most of your income, but you keep a small Personal Expenses Allowance.

Be aware that Scotland, Wales, and Northern Ireland have their own distinct capital limits and funding rules.

Self-Funding: Paying for Care from Your Own Resources

If your capital is above the upper limit, you are classified as a 'self-funder'. You are responsible for arranging and paying your own nursing home fees. Common methods for funding include using income from pensions, drawing on savings and investments, or using funds from a property sale. The process of Paying for a care home can feel complex, and if it involves selling a property, expert guidance from an experienced estate agent is invaluable. To understand the process in a specific local market, you can learn more about Spire Vue Estates, an agency that provides guidance for buyers and sellers in the North East. Crucially, even as a self-funder, you are still entitled to a free care needs assessment from your council to determine the level of care you require.

Exploring Funding Support, Benefits, and Ways to Pay

When considering how much are nursing home fees UK wide, it is vital to explore all available funding. Several government, NHS, and local authority schemes can substantially reduce your personal contribution. Understanding your eligibility for these is a critical first step in managing the cost of care.

NHS Continuing Healthcare (CHC)

NHS Continuing Healthcare is a package of care fully funded by the NHS. It covers all care fees, including accommodation, for individuals with a 'primary health need'. This means their main need for care is due to health-related issues, not social care. Eligibility is not based on a specific diagnosis but on a detailed assessment of needs. Qualifying for CHC is difficult, but if successful, it removes the financial burden of care entirely.

NHS-Funded Nursing Contribution (FNC)

If you do not qualify for CHC but have been assessed as needing care from a registered nurse, you may be eligible for the NHS-Funded Nursing Contribution (FNC). This is a non-means-tested, flat-rate weekly payment made directly to the nursing home to reduce your fees. For 2023-2024 in England, the rate is £219.71 per week. An NHS nurse must assess your needs to confirm your eligibility for this contribution.

Benefits: Attendance Allowance and Pension Credit

Certain state benefits can be used to help pay for nursing home fees. It is essential to check your entitlement for everything available. Key benefits include:

- Attendance Allowance: A non-means-tested benefit for individuals over the State Pension age who have a disability or illness that requires help with personal care.

- Pension Credit: A means-tested benefit that tops up the weekly income of low-income pensioners to a minimum level.

A full benefits check with an organisation like Age UK or Citizens Advice is highly recommended.

Deferred Payment Agreements: Delaying Selling a Home

Many people fear they must sell their home immediately to pay for care. A Deferred Payment Agreement with your local council can prevent this. This scheme is effectively a loan against the value of your property. The council pays a portion of your care home fees, and the loan is repaid, with interest, when the property is eventually sold. Eligibility criteria apply, and you should seek independent financial advice before entering an agreement.

Explore all your funding options to get a clear picture of your financial situation. You can find more detailed information and resources at guide2care.com.

Your 4-Step Plan for Managing Nursing Home Fees

Navigating the costs of care can be complex. This straightforward plan breaks down the process into four manageable steps, providing a clear path from initial assessment to finding the right home. Following these actions will help you find a definitive answer to the question of how much are nursing home fees uk for your specific situation.

Step 1: Request a Free Care Needs Assessment

Your first action is to contact the adult social services department at your local council. Request a free care needs assessment for the person requiring care. This evaluation determines the specific level of support needed, from personal care to 24-hour nursing. It is based entirely on need, not financial circumstances, and is the essential first step to accessing any council support.

Step 2: Complete the Financial Assessment (Means Test)

If the needs assessment shows that a nursing home is required, the council will then offer a financial assessment, often called a means test. You will need to provide detailed information about income, savings, and assets. Prepare key documents in advance, such as:

- Bank and building society statements

- Details of private or state pensions

- Information on any property or investments

This assessment provides a clear result on whether you qualify for local authority funding and how much you may need to contribute towards the fees.

Step 3: Seek Independent Financial Advice

Understanding how to pay for long-term care is a significant financial decision. We strongly recommend consulting an independent financial adviser who specialises in care fees planning. They are qualified to explain your options in detail, which could include products like immediate needs annuities or equity release. This professional guidance is crucial for making a sustainable and informed choice, particularly if you will be self-funding. As part of this broader financial review, many also consider how life insurance fits into their estate; resources such as LifeInsure.com allow you to compare term life insurance quotes instantly. For families whose long-term planning also involves international options, such as moving to be closer to relatives abroad, you can explore Immigration Consultations (via partners) to understand the requirements. To see an example of how alternative assets can fit into a long-term financial strategy, you can visit Whisky Cask Club.

Step 4: Find and Compare Local Nursing Homes

Once you have a clear understanding of your budget from the means test and financial advice, you can begin your search for a suitable home. It is vital to find out exactly what is included in the fees. Shortlist several providers, arrange visits, and always request a detailed, written quote that breaks down all costs, including any potential extras. This ensures you can accurately compare homes and avoid unexpected charges.

Use our directory to find nursing homes in your area and compare their services.

Find the Right Nursing Home at the Right Price

Navigating the cost of care begins with a clear understanding of the key factors involved. As we have outlined, the answer to how much are nursing home fees UK-wide depends heavily on the specific care needs of the individual and the location of the home. Acknowledging this variability is the first step. The second is to thoroughly investigate all potential funding streams, including local authority support, NHS funding, and any benefits you may be entitled to. This creates a solid foundation for your financial planning.

With this knowledge, you are ready to take the next practical step: comparing specific nursing homes. Guide2Care is designed to make this process straightforward. Our comprehensive UK-wide listings provide free, impartial information on homes across the country. Use our simple filters to search by care type, location, and official CQC rating, giving you the clarity needed to make a confident and informed decision.

Find The Care You Need. Search our directory to compare nursing homes and their fees today.

Frequently Asked Questions

Do you always have to sell your home to pay for a nursing home in the UK?

No, you do not always have to sell your home. The value of your property is not included in the financial assessment if your partner, a relative over 60, or a disabled relative will continue to live there. This is known as a property disregard. Additionally, for self-funders entering care, councils offer a 12-week property disregard period. This gives you time to decide how to pay for long-term care without having to sell your home immediately.

What happens if my savings run out while I'm in a nursing home?

You will not be asked to leave the care home if your savings are depleted. Once your capital falls below the upper threshold (£23,250 in England), you can apply for local authority funding. You must contact your council for a financial reassessment before your savings reach this level. The council will then assess your eligibility for support and, if you qualify, will begin contributing towards the cost of your care fees according to their standard rates.

Can a nursing home increase its fees after I move in?

Yes, most nursing homes can and do increase their fees. This is typically done annually to account for inflation, rising operational costs, and staff wage increases. Your contract with the care provider must clearly state the terms for any fee reviews, including how and when they will occur and the amount of notice you will receive. It is vital to review this section of the contract carefully before you sign to understand potential future costs.

What is a 'third-party top-up fee' and when is it required?

A third-party top-up fee is an additional payment made to cover the difference between the amount a local authority will pay for care and the actual cost of a chosen nursing home. It is required when a person is eligible for council funding but selects a home that is more expensive than the council's standard rate. This fee must be paid by a third party, such as a family member or charity, and not from the resident's own capital if it is below the upper savings threshold.

Are nursing home fees tax-deductible in the UK?

In most circumstances, nursing home fees are not tax-deductible for the individual paying them. There is no general tax relief available for care costs paid out of your personal income or savings. The only component of care funding that is tax-free is NHS-funded Nursing Care (FNC). This is a non-means-tested benefit paid directly to the nursing home to cover the cost of nursing care from a registered nurse, not the accommodation fees.

How is income from pensions and benefits treated in the financial assessment?

During a local authority financial assessment, nearly all forms of regular income are taken into account. This includes your State Pension, private or occupational pensions, and most welfare benefits. However, certain benefits, such as the mobility component of the Personal Independence Payment (PIP), are disregarded. After assessing your income, you will be left with a weekly Personal Expenses Allowance (PEA) for your own use, with the remainder going towards your care fees.