Self-Funding Care Home Fees Advice: A Complete 2026 Guide

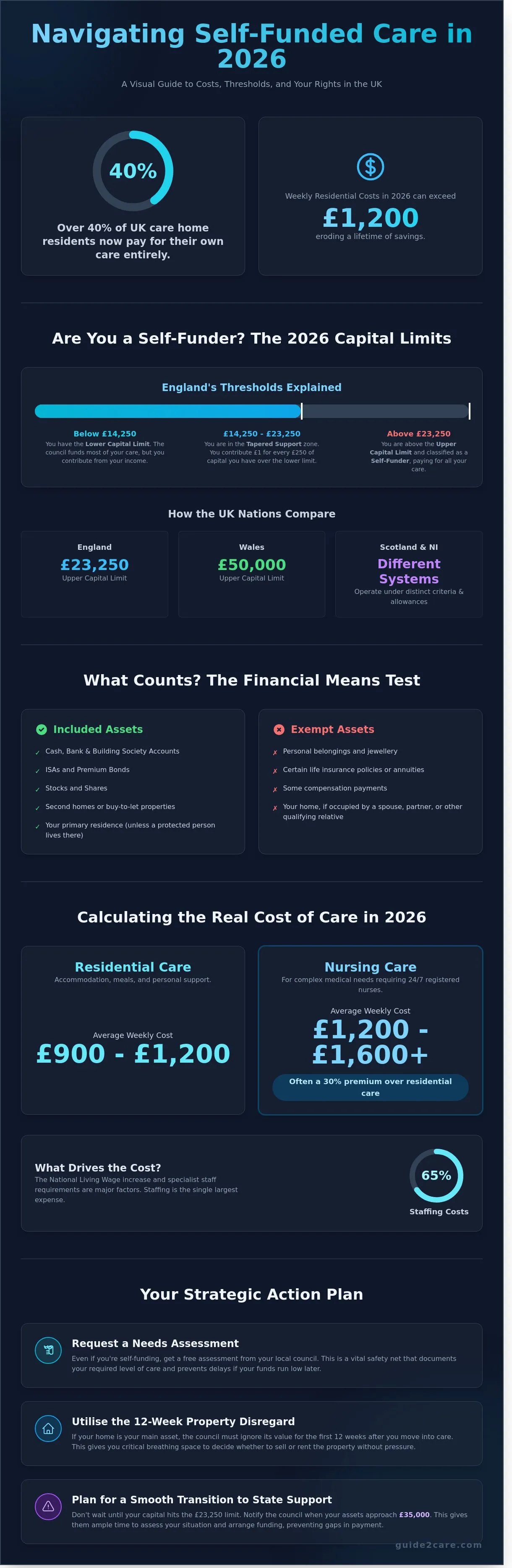

Did you know that over 40% of residents in UK care homes now pay for their own support entirely out of their own pockets? With weekly residential costs in 2026 often exceeding £1,200, finding reliable self-funding care home fees advice is the only way to ensure your finances remain sustainable. It's natural to feel concerned about the speed at which care costs can erode a lifetime of savings or an intended inheritance. You've worked hard for your assets, and the thought of them vanishing into monthly invoices is understandably stressful.

We'll show you exactly how to manage these costs while protecting your interests. This guide clarifies the 2026 capital limits for England, Scotland, and Wales, which remain frustratingly different depending on your postcode. You'll learn about non-means-tested benefits you're entitled to receive regardless of your total wealth. We also provide a clear strategy for handling property assets and avoiding common financial pitfalls. Use this information to take control of your care journey and find the stability you need.

Key Takeaways

- Identify the 2026 upper capital limit of £23,250 and understand how your savings and property impact your status as a self-funder.

- Get practical self-funding care home fees advice to navigate 2026 average weekly costs and spot hidden charges in private care contracts.

- Compare the financial implications of selling versus renting the family home while utilising the 12-week property disregard for financial breathing space.

- Learn how to negotiate fair care terms and understand your legal rights when dealing with private providers.

- Plan for a smooth transition to state support by identifying the exact point to notify the council when assets approach £35,000.

Understanding Self-Funding in 2026: Thresholds and Rules

A self-funder is an individual who pays the full cost of their social care services. In the 2026 UK care system, this status is usually determined by a financial assessment. You are classified as a self-funder if your qualifying capital exceeds the government's upper limit. This means you're responsible for arranging your care and meeting all monthly invoices from residential or nursing home providers. If you require specific self-funding care home fees advice, start by calculating the total value of your liquid and fixed assets to see where you stand against current thresholds.

England maintains an upper capital limit of £23,250 for 2026. If your savings, investments, or property value exceed this figure, the local authority won't contribute to your care costs. The legal framework governing these rules is complex, so Understanding the social care system in England is helpful for grasping how the Care Act 2014 dictates local authority responsibilities. While the £23,250 limit is the standard for England, other parts of the UK apply different rules. For instance, Wales currently uses a higher capital limit of £50,000 for residential care, while Scotland and Northern Ireland operate under their own distinct assessment criteria and personal care allowances.

The 2026 Capital Limits Explained

The financial assessment, or means test, looks at almost everything you own. In 2026, the £23,250 threshold remains the primary trigger for self-funding. Assets included in this calculation are your bank and building society accounts, National Savings accounts, stocks, shares, and any second homes or buy-to-let properties. Your primary residence is also included if you're moving into a care home, unless a spouse, partner, or a dependent relative over 60 years old still lives there. Some assets remain exempt, such as certain types of life insurance policies or specific compensation payments. The means test is a mandatory step for anyone seeking future state support to determine their financial eligibility.

- Upper Limit (England): £23,250.

- Lower Limit (England): £14,250 (below this, the council pays more, but you still contribute from income).

- Included Assets: Cash, ISAs, premium bonds, and property (with exceptions).

- Exempt Assets: Personal belongings, certain annuities, and property occupied by a protected person.

Why Seek a Needs Assessment if You Are Self-Funding?

Even if you're certain your capital is well above the £23,250 limit, you should still request a Needs Assessment from your local council. This document provides an official benchmark of the specific type and level of care you require. It's a professional evaluation that ensures you're looking for the right kind of facility, whether that's a residential home or a specialized nursing unit. Seeking professional self-funding care home fees advice early ensures you don't overpay for services that might be partially funded or unnecessary for your condition.

This assessment acts as a vital safety net. If your funds eventually dwindle below the £23,250 threshold, the local authority will need to take over some or all of the funding. Having a prior Needs Assessment on file speeds up this transition significantly. It prevents delays in funding that could otherwise lead to debt or the threat of eviction. Local authorities have a legal duty to provide this assessment for free to anyone who appears to need care, regardless of their financial situation. Use this service to document your requirements and protect your future financial security.

Calculating the Real Cost of Care in 2026

Care costs in 2026 reflect a sharp rise in operational overheads and staffing requirements. Staffing costs now account for approximately 65% of a care home's total expenditure. The April 2026 National Living Wage increase has pushed baseline fees higher than previous years. When seeking self-funding care home fees advice, you must account for these inflationary pressures. Total monthly invoices often exceed initial estimates because families overlook the distinction between basic accommodation and clinical support.

Residential vs. Nursing Home Fees

Residential care provides accommodation, meals, and personal care such as dressing or bathing. In 2026, the UK average for residential care sits between £900 and £1,200 per week. Nursing care is significantly more expensive. It requires registered nurses to be on-site 24 hours a day to manage complex medical needs. Expect to pay between £1,200 and £1,600+ per week for nursing provision. This 30% premium covers clinical equipment, professional insurance, and higher staff-to-resident ratios. Always ask for a breakdown of the "Nursing Care Contribution" to see how much the NHS covers toward these clinical costs.

Regional Price Variations

Location is the primary driver of price disparity across the UK. The "South East premium" remains a dominant factor in 2026. A standard residential room in Surrey or North London often costs £1,550 per week. In contrast, similar facilities in the North East or West Midlands average £850 to £1,000. This 45% price gap means a self-funder in the South will deplete their assets nearly twice as fast as someone in the North. Research local market rates thoroughly before committing to a contract. You can compare regional providers to find options that align with your long-term budget.

The Impact of Dementia Specialisms

Dementia care adds another layer of cost to the monthly invoice. Specialized memory care units require specific architectural designs and higher staffing levels to ensure resident safety. In 2026, dementia specialisms typically add £150 to £300 to the standard weekly residential fee. These costs cover staff training in behavioral management and the maintenance of secure sensory gardens. If a resident's needs escalate from standard residential to dementia-specific care, the home will trigger a fee review. Ensure the initial contract specifies how these transitions affect your weekly rate.

Watch Out for Hidden Surcharges

Contracts often contain "hidden extras" that are not included in the headline weekly rate. Self-funders frequently overlook these costs during the initial transition. Common surcharges include:

- Admin or Community Fees: Upfront charges ranging from £1,000 to £3,500 for "processing" the move.

- Accompanied Visits: Charges for staff to take residents to hospital appointments, often billed at £25 per hour.

- Personal Services: Hairdressing, chiropody, and specialized dental care.

- Laundry: Some homes charge extra for dry cleaning or delicate garment care.

Review the "fee increase" clause in your 2026 contract. Most providers now link annual increases to the Consumer Price Index (CPI) plus a fixed percentage, usually 2% or 3%. Understanding how to pay for a care home involves projecting these increases over a five-year period to ensure your capital remains sufficient. Clear self-funding care home fees advice suggests keeping a contingency fund of at least 10% above the quoted annual rate to cover these inevitable surcharges.

Strategic Funding Options: Protecting Your Assets

Deciding how to manage the family home is the most significant hurdle when organising care. You must choose between selling the property or renting it out to generate income. Renting can provide a steady stream of capital, often between £900 and £1,500 per month depending on the region. However, you must factor in 20% or 40% income tax, maintenance costs, and letting agent fees. Selling releases a large lump sum immediately, which allows for more flexible investment options. Use professional self-funding care home fees advice to calculate which route preserves your capital for longer.

To ensure the capital you release or the income you generate is working as hard as possible, it's wise to shop around for the best rates on financial products. For a straightforward way to compare your options, you can check out RatesChaser.

Of course, another strategy is to find support that allows a senior to remain in their own home, avoiding the need to sell or rent it out. While their services are based in Canada, looking at the comprehensive support offered by providers like Cocoon Senior Services can give families ideas on how non-medical home care can delay or prevent the need for a residential move.

Similarly, some individuals look beyond the UK for their retirement planning, where their assets might stretch further. For those interested in how far-reaching this planning can be, it's useful to see what's involved in retiring to a popular destination like Thailand. You can discover Expat Retirement Chronicles for a detailed look at this process.

Beyond long-term relocation, some individuals choose to use their savings for significant life experiences while they can. For those who have always dreamed of exploring the world in style, a journey on a luxury train in South India can be an unforgettable way to create lasting memories.

The 12-week property disregard provides an essential financial cushion. Local authorities must ignore the value of your home for the first 12 weeks after you move into permanent residential care. This rule applies if your other savings are below the £23,250 threshold. It prevents a forced "fire sale" of your home, giving your family time to arrange a better sale price or set up a rental agreement. During this period, the council helps with costs, but you must still contribute from your pensions or other income.

Be aware of the Deprivation of Assets rules. Local authorities investigate any large gifts or property transfers made to avoid paying for care. There's no "seven-year rule" like there is for Inheritance Tax. If a council decides you gave away assets with the intention of reducing your care costs, they will assess you as if you still own those assets. This can lead to a total withdrawal of state support and legal complications for the person who received the gift.

The Deferred Payment Scheme (DPS)

A Deferred Payment Scheme acts as a loan from your Local Authority. The council pays your care home fees and secures the debt against your property. You don't have to sell your home during your lifetime. To be eligible in 2026, your capital excluding the property must be below £23,250. The council performs a "sustainability check" to ensure the property value covers the loan and interest for the duration of your care. Interest rates are currently set around 4.05%, and administrative fees for setting up the legal charge can exceed £500. For more details, consult NHS advice on self-funding care.

Non-Means-Tested Benefits for Self-Funders

Every self-funder should claim Attendance Allowance. This benefit is not means-tested and is available to those over state pension age who need help with personal care. In 2026, the lower rate is approximately £72.65 per week, while the higher rate for those requiring day and night care is £108.55 per week. Claiming this can provide over £5,600 a year towards your fees. If you're under pension age, you should apply for Personal Independence Payment (PIP) instead.

NHS Funded Nursing Care (FNC) is another vital resource for those in nursing homes. If a registered nurse is required to provide or supervise your care, the NHS pays a flat rate directly to the care home. For 2024/25, this rate is £235.88 per week, and it's expected to rise by 2026. Always check your care home contract to ensure this payment reduces your gross fee rather than being kept by the provider as an extra. Following specific self-funding care home fees advice ensures you don't miss out on these automatic entitlements.

The Self-Funder's Rights and Contractual Guidance

Entering a care home is a significant financial commitment. As a self-funder, you're a consumer with specific legal protections. The Care Quality Commission (CQC) and the Competition and Markets Authority (CMA) regulate how providers present their costs. Since 2024, the CQC has tightened its monitoring of fee transparency. Providers must now provide clear, upfront information about their pricing structures before you visit. This regulatory shift ensures you can compare services without hidden charges. Understanding your rights is the first step in securing self-funding care home fees advice that protects your long-term capital.

A fair care contract in 2026 should be easy to read. It must clearly list what the weekly fee covers and what it doesn't. Standard inclusions usually cover accommodation, meals, laundry, and 24-hour care. Always check the "additional extras" section. Some homes charge separately for chiropody, hairdressing, or accompanied hospital visits. If these costs aren't explicitly stated, you shouldn't pay them. You also need to be aware of "Third-Party Top-Ups." While these are common for local authority funded residents, self-funders should ensure their family members aren't being asked to pay extra for services that the primary fee already covers.

Negotiating Your Care Fees

You have the power to negotiate. Many private care homes operate like businesses and have occupancy targets. If a home has an occupancy rate below 85%, they may offer a discount to fill the room. Request an "occupancy discount" or a "new starter rate" for the first 12 months. You should also ask for a fixed-fee period. Secure a written agreement that fees won't rise for at least the first year of residency. This protects you from mid-year inflationary spikes. Ensure every verbal promise made during a tour is written into the final contract. Verbal agreements are difficult to enforce if disputes arise later.

This business-oriented approach is part of a larger, specialized industry. While the UK market has its own dynamics, the buying and selling of care facilities is a global business. In the US, for instance, specialized firms like Healthcare Biz Brokers, Inc. facilitate these complex transactions, highlighting how the senior care sector operates on commercial principles. Understanding this broader context can empower families to see themselves as valued customers in a competitive market.

Understanding Termination and Notice Periods

Standard notice periods for self-funders are usually 28 days. This period allows you time to find alternative care if the current environment isn't suitable. Be cautious of contracts that demand longer notice periods, as these can be deemed unfair under CMA guidance. You must also review the "fees after death" clause. The CMA's 2018 ruling states that providers can only charge fees for a maximum of three days after a resident passes away, or until the room is cleared, up to a maximum of ten days. Anything longer is likely an unenforceable term.

- Check if the weekly fee reduces if the resident is admitted to hospital for more than 7 days.

- Look for a "room retention" discount, which is typically 10% to 20% off the standard rate.

- Confirm how long the home will hold the room before they consider the contract terminated.

- Verify if care-related costs, such as 1-to-1 support, are deducted while the resident is away.

Reviewing the small print prevents unexpected bills. If a contract seems one-sided, ask for it to be amended before you sign. Providers are often willing to make minor adjustments to secure a long-term resident. Use our resources to find the care you need and compare provider terms effectively.

Planning for the Future: When Self-Funding Ends

Self-funding care doesn't always last forever. Capital levels fluctuate as care needs intensify or annual fees increase. In England, the threshold for state support begins when your assets fall below £23,250. You shouldn't wait until you reach this exact figure to take action. Local authorities often take 12 to 16 weeks to process assessments and finalise funding agreements. This timeframe can create a stressful gap if your funds run dry before the council steps in.

Practical self-funding care home fees advice suggests contacting your local council when your total assets reach approximately £35,000. This provides a buffer of roughly £11,750 above the upper limit. It ensures your financial assessment is complete and your care needs are officially documented before you hit the £23,250 mark. If you delay this notification, you might face a period where you can't afford the private rate but the council hasn't yet authorised payments.

The Transition to State Support

Moving from private funding to local authority support involves three specific steps. First, request a new financial assessment from the council 3 to 6 months before your capital hits £23,250. Second, ask for the council's 'usual cost' or standard rate for the required care level. Third, speak with the care home manager. Negotiate to see if they'll accept the council's rate to keep the resident in their current room without requiring an additional top-up fee.

The Top-Up Fee Challenge

A common issue arises if the care home's private rate is significantly higher than what the council is willing to pay. This creates the 'top-up' trap. If the council offers £850 per week but the home charges £1,150, a £300 gap exists. Usually, the resident cannot pay this from their remaining savings, which are protected below £14,250. A family member or a charitable organisation must provide a 'third-party top-up' to cover the difference. If no one can pay this, the resident might be forced to move to a more affordable room or a different facility that accepts the standard local authority rate.

Finding the Right Match with Guide2Care

Preparation is the best way to avoid a forced move later. Use the Guide2Care directory to identify providers that work with local authorities from the outset. You can filter your search by care type, location, and CQC rating to ensure quality standards. Look for listings featuring 'transparent pricing' badges. These providers offer clearer breakdowns of their fee structures, helping you calculate exactly how long your capital will last. This data allows you to choose a home that is likely to accept council rates in the future, providing long-term stability. Find the care you need by exploring our UK directory today.

Planning for the end of self-funding is a vital part of self-funding care home fees advice. By understanding the £23,250 and £14,250 thresholds, you can manage your transition effectively. Ensure you keep copies of all bank statements and property valuations to speed up the council's means test. This proactive approach protects the resident from unnecessary disruption and ensures continuity of care when the state begins to contribute.

Take Control of Your 2026 Care Planning

Navigating the UK care system in 2026 requires a clear understanding of the £23,250 and £14,250 capital thresholds. You've explored how to calculate the true cost of residential support and how to protect your assets through informed legal choices. Expert self-funding care home fees advice helps you manage these financial commitments while ensuring your contractual rights are fully protected. It's vital to monitor your remaining capital to prepare for the point where local authority assistance becomes available.

Start your search for a suitable provider now. You can find the care you need in our comprehensive UK directory. We provide a structured resource featuring detailed care provider profiles and integrated CQC ratings for every location. This tool allows you to compare facilities across the country using verified data and transparent information. You'll find the right balance of quality and cost-effectiveness for your specific situation. Making an informed choice today provides peace of mind for the years ahead.

Frequently Asked Questions

Can the council force me to sell my home to pay for care home fees in 2026?

The local authority cannot force you to sell your home during your lifetime to pay for care. In 2026, you can use a Deferred Payment Agreement to secure care costs against your property value. This legal arrangement means the council pays your fees and recovers the money once the house is eventually sold. If a spouse or a relative aged over 60 still lives in the property, the council must disregard its value entirely.

How much money can I keep if I am self-funding my care?

You can keep a minimum of £14,250 in capital and savings under current UK assessment rules. If your assets exceed £23,250, you're responsible for the full cost of your residential care. When your savings fall between these two figures, the local authority provides partial funding. These thresholds apply to your individual assets and don't include your partner's share of joint accounts or property.

Is Attendance Allowance means-tested for care home residents?

Attendance Allowance is not means-tested and stays available to self-funders regardless of their income or savings. You can receive either £72.65 or £108.55 per week depending on the level of care you need. If the local authority starts contributing to your care home fees, this benefit usually stops after 28 days. You must notify the Department for Work and Pensions when you move into a care facility.

What happens if I run out of money while in a care home?

You should contact your local council for a new financial assessment once your assets drop towards the £23,250 threshold. They'll then determine if you qualify for state support to cover your ongoing costs. It's vital to seek professional self-funding care home fees advice at least six months before your funds reach this limit. This preparation ensures a smooth transition and prevents you from accruing personal debt with the care provider.

Can I give my house to my children to avoid paying care fees?

You can gift your home to your children, but the council may treat this as a deprivation of assets. If the local authority decides you gave away property to avoid care costs, they'll assess your finances as if you still own the house. There's no seven-year rule for care fees like there is for Inheritance Tax. They look at your intent and the timing of the gift relative to your need for care.

What is the average cost of a care home in the UK in 2026?

Average residential care costs in the UK are projected to reach £1,100 per week by 2026. For those requiring nursing care, weekly fees will likely average £1,450 across England and Wales. These figures represent a 15% increase from 2024 levels based on current social care inflation trends. Costs vary significantly by region, with London and the South East often charging 25% more than the national average.

Do I have to pay for my own nursing care if I have medical needs?

You don't have to pay for the nursing element of your care if a registered nurse provides it. The NHS pays a flat rate called NHS Funded Nursing Care, which is currently £235.88 per week in England. If your needs are primarily health-based rather than social, you might qualify for NHS Continuing Healthcare. This funding covers 100% of your care home fees, including accommodation and board.

How often can a care home increase their fees for self-funders?

Care homes typically increase their fees once every 12 months, usually in April to match the new financial year. Providers must give you at least 28 days' written notice before any price change takes effect. Your contract should clearly explain how they calculate these increases, often linking them to the Consumer Price Index or specific staff wage rises. Review your agreement for professional self-funding care home fees advice and to see if there's a cap on annual percentage hikes.