What Happens When Savings Run Out in a Care Home? A UK Guide for 2026

Does reaching the lower capital limit mean your loved one must move to a cheaper room immediately? You likely feel the pressure of depleting funds and the complex paperwork required by your local authority. It's a common concern that once private funds fall below £23,250, the care home might issue an eviction notice. This guide details exactly what happens when savings run out in a care home uk, outlining your legal protections and the mandatory financial assessments for 2026.

You can secure the continuity of care by understanding the transition from self-funding to state support. We provide a clear timeline for when to notify the council, which is typically when capital reaches the £23,250 threshold. This article explains the 12-week property disregard rules and the specific conditions under which a resident can remain in their current home. You'll also find a breakdown of how top-up fees work to ensure you aren't paying more than the law requires.

Key Takeaways

- Identify the 2026 Upper and Lower Capital Limits to determine exactly when state-funded tapered support begins.

- Learn why initiating a financial assessment when capital hits £35,000 is critical for a smooth transition from self-funding.

- Understand the "Continuity of Care" principle to see what happens when savings run out in a care home uk and if a resident can be forced to move.

- Explore the legal regulations surrounding third-party top-up fees and how to access potential NHS funding streams.

- Use the Guide2Care directory to find high-quality providers that accept local authority rates to secure your long-term care strategy.

Understanding UK Care Funding Thresholds and Capital Limits in 2026

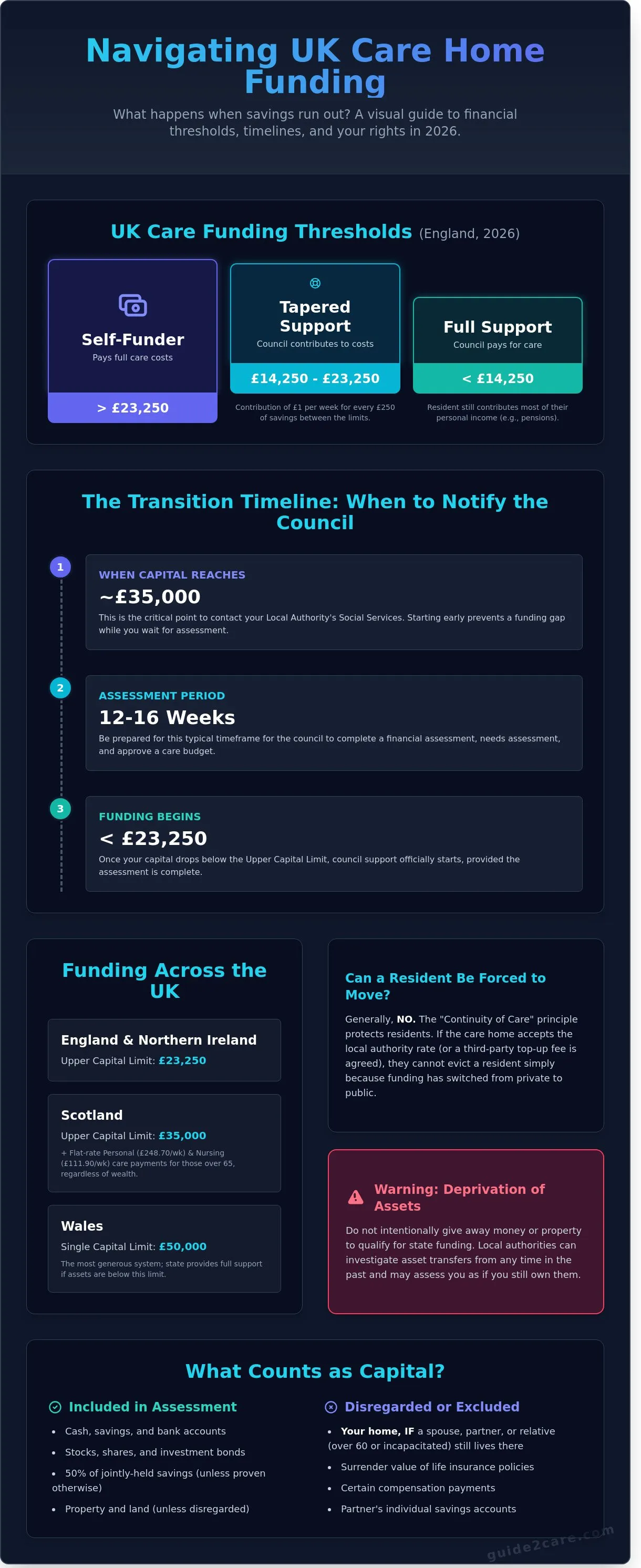

UK care funding relies on specific financial thresholds known as the Upper Capital Limit (UCL) and the Lower Capital Limit (LCL). These figures determine who qualifies for state support and who must pay for their own care. As of 2026, the UCL in England remains at £23,250. If your assets exceed this amount, you're classified as a "self-funder" and must pay the full cost of your residency. The LCL is set at £14,250. If your capital falls below this lower limit, the local authority usually pays for your care, though you'll still contribute most of your personal income, such as pensions.

Understanding Social care in England is essential because these rules only apply to social care, not medical care. If your primary needs are health-based, you might qualify for NHS Continuing Healthcare, which is free regardless of your savings. Between the UCL and LCL, you enter a "tapered support" zone. Here, the council provides partial funding, but they'll charge you a "tariff income" of £1 per week for every £250 of savings you have between the two limits. Knowing what happens when savings run out in a care home uk helps you prepare for the moment your capital hits these specific markers.

To better understand how these financial thresholds work in practice, watch this helpful video:

Local authorities treat joint bank accounts and shared assets with specific rules. Usually, they assume you own 50% of any joint account unless you can prove otherwise. They won't look at your partner's individual savings, but they'll examine any shared capital to ensure the means test is accurate. This distinction is vital for couples who want to protect the financial stability of the partner staying at home.

Regional Variations: England, Scotland, Wales, and Northern Ireland

Care funding isn't uniform across the UK. In England and Northern Ireland, the UCL is £23,250. Scotland offers a different system where the UCL is £35,000. Crucially, Scotland provides a flat-rate "Personal Care" payment of approximately £248.70 per week and a "Nursing Care" payment of £111.90 per week to everyone aged 65 and over, regardless of wealth. Wales is currently the most generous, with a single capital limit of £50,000 for residential care. If your assets are below £50,000 in Wales, the state provides full financial support for your care costs.

What Counts as Capital? Savings, Pensions, and Property

The means test includes most forms of wealth, including cash, stocks, and investment bonds. However, the "Property Disregard" rule is a vital protection. Your home isn't counted in the means test if your spouse, partner, or a relative who is over 60 or incapacitated still lives there. This ensures that what happens when savings run out in a care home uk doesn't result in a partner losing their home. Certain assets are also excluded, such as the surrender value of life insurance policies and specific compensation payments.

This makes it a good time for seniors to explore Final Expense Life Insurance, which can help cover funeral costs without affecting their eligibility for care funding.

You must also be aware of "deprivation of assets" rules. Local authorities check if you've intentionally given away money or property to qualify for state funding. There's no time limit on how far back they can look. If they decide you've deliberately reduced your capital to avoid fees, they may assess you as if you still own those assets. This can lead to significant legal and financial complications during the funding application process.

The Transition Timeline: When to Notify the Local Authority

Start the application process for state support when the resident's capital drops to approximately £35,000. While the upper capital threshold for local authority funding in England is £23,250, you shouldn't wait until you reach this figure. The administrative transition from self-funding to state-funded care is rarely instant. It frequently takes between 12 and 16 weeks for a local authority to complete the necessary assessments and approve a budget.

Notifying the council early helps prevent a funding gap. This gap occurs when a resident's savings fall below the threshold, but the council hasn't yet authorised payments. In these cases, the care home may still demand the full private rate, leaving the family to cover the shortfall. Understanding what happens when savings run out in a care home uk is vital for financial stability. Contact the Social Services "Financial Assessment" team to log your intent to claim support well in advance of hitting the limit.

Keep meticulous records of all care-related expenditure. The council will scrutinise bank statements from the previous 12 to 24 months to ensure capital wasn't deliberately reduced. This process, known as investigating "deprivation of assets," looks for large gifts or unusual spending. Detailed records of care fees, utility bills, and personal expenses provide the evidence needed to clear this check. For a clearer picture of these rules, consult the Age UK guide to paying for a care home which details the legal obligations of the local authority.

Step 1: Requesting a New Needs Assessment

The council won't provide funding based on your current private arrangement alone. They must conduct a fresh Care Needs Assessment. This is a formal review by a social worker to confirm the resident’s physical or cognitive needs still justify a residential placement. If the assessment suggests the resident's needs have decreased, the council might argue that a cheaper home care package is more appropriate. You must provide evidence from GPs or care home staff to prove that 24-hour residential care remains the only safe option.

Step 2: The Financial Means Test

Once the need for care is established, the council performs a financial means test. You'll need to submit several documents, including three months of bank statements, DWP pension letters, and proof of any private annuities. The council uses this data to calculate the "resident contribution." Most of the resident's income, such as their State Pension, will go toward the care costs, leaving them with a Personal Expenses Allowance of £30.15 per week. If the resident owns a property that's currently on the market, the council applies a 12-week property disregard. During these 84 days, the value of the home is ignored, and the council provides temporary funding to bridge the gap until the house sells.

Managing this transition requires careful planning and constant communication with the local authority. If you're currently looking for facilities that accept local authority rates, you can find the care you need using our comprehensive directory. This ensures you're prepared for the next stage of the funding journey.

Can a Resident Be Forced to Move if the Council Pays Less?

The prospect of moving to a cheaper facility is the most common concern for families asking what happens when savings run out in a care home uk. Local authorities often suggest a relocation if the current home's fees exceed the council's standard budget. However, residents possess legal protections that prevent arbitrary moves. Understanding what happens when savings run out in a care home uk involves knowing that the council cannot simply ignore your existing care arrangements or health status.

The Care Act 2014 establishes the "Continuity of Care" principle. This means a local authority cannot force a move simply to save money if the transition would negatively impact the resident's health. The council must conduct a formal assessment before proposing a move. They have to prove that the new home can meet all identified care needs and that the move itself won't cause physical or psychological harm. For residents with advanced age or frailty, the risks of "transfer trauma" often outweigh the financial benefits of a cheaper bed.

The Local Authority "Usual Cost" vs. Private Rates

Each council sets a "usual cost" or "standard rate," which is the maximum amount they expect to pay for a specific type of care. These rates are determined by local market assessments. Private rates for self-funding residents are typically 25% to 50% higher than these council figures. This occurs because private fees often subsidise the lower rates paid by the state. If your savings drop below the £23,250 threshold, the council must step in. They are legally required to provide at least one care home option that fits within their standard rate. If the current home costs more, the council may ask for a third-party top-up fee from a relative to cover the difference.

Challenging a Forced Relocation

You can challenge a decision to move a resident by providing clinical evidence. A letter from a GP or a geriatric consultant is the most effective tool. This evidence should explicitly state that a relocation would cause detrimental effects to the resident's health. This is particularly vital for residents with dementia, where familiarity with surroundings and staff is a core component of their care plan. If a resident has nursing needs, NHS-funded nursing care provides £235.88 per week (2024/25 rate) to help cover costs, which might bridge the gap between council rates and private fees.

If the council ignores clinical advice, you can escalate the matter to the Local Government and Social Care Ombudsman. They investigate whether the council followed proper procedures and respected the resident's rights. The well-being principle is a legal requirement under Section 1 of the Care Act 2014 that compels local authorities to promote an individual's physical, mental, and emotional health in every decision they make.

Closing the Gap: Top-up Fees and NHS Funding Options

Local authorities in England set a maximum budget for care based on their "usual cost" for a room. If your preferred care home charges £1,200 per week but the council only pays £850, a funding gap exists. This shortfall is typically managed through a third-party top-up fee. When considering what happens when savings run out in a care home uk, you must understand that the council is only obligated to fund a room that meets your assessed needs, not necessarily your current room.

A third-party top-up is a payment made by someone other than the resident, usually a family member, friend, or charity. The payer must sign a legal agreement with the local authority. This person takes on the financial responsibility for the difference between the council's budget and the care home's actual fees. It's a long-term commitment that requires careful budgeting.

Residents cannot usually pay their own top-up fees from their remaining capital. Once your savings drop below the £23,250 threshold, the council expects your remaining assets, down to the £14,250 lower limit, to be protected for personal expenses. Using this "protected" money for fees is generally prohibited under Department of Health and Social Care (DHSC) guidelines. The only exception is if you have a 12-week property disregard or a deferred payment agreement in place.

Entering into a top-up agreement carries significant risks. If the family member can no longer afford the payments, the care home is not required to absorb the loss. In these cases, the resident may be forced to move to a cheaper room or a different facility entirely. Data from the 2023 care sector reports show that top-up fees can range from £50 to over £500 per week, making them a major financial burden for families.

NHS Funded Nursing Care (FNC) Explained

NHS Funded Nursing Care (FNC) is a flat-rate weekly payment for people who need registered nursing care in a care home. For the 2024/25 financial year in England, the standard rate is £235.88 per week. This payment is not means-tested. It's available to everyone who requires nursing intervention, regardless of whether they are a self-funder or council-funded.

The NHS pays FNC directly to the care home provider. This payment is intended to cover the cost of the nursing staff's time. For self-funders, this often results in a direct reduction of the gross weekly fee. You should check your contract to ensure the FNC amount is clearly deducted from your monthly invoice.

NHS Continuing Healthcare (CHC): The "Holy Grail" of Funding

NHS Continuing Healthcare (CHC) is a package of ongoing care that is 100% funded by the NHS. It covers both health and social care costs, including care home accommodation fees. To qualify, you must be assessed as having a "primary health need." This means your needs are complex, intense, or unpredictable, and go beyond what a local authority is legally allowed to provide.

The assessment follows a strict two-stage process. First, a healthcare professional completes a "Checklist" to see if you trigger a full assessment. If you pass this stage, a Multi-Disciplinary Team (MDT) performs a comprehensive review of your health needs. This assessment is a vital step in managing what happens when savings run out in a care home uk, as it removes the burden of means-testing entirely. You should request a CHC screening as soon as care needs increase, preferably before your capital hits the £23,250 mark.

Next Steps: Organising Your Care Strategy with Guide2Care

Transitioning from self-funding to local authority support requires a proactive approach to administration. You should begin this process when your assets fall towards the £23,250 threshold, as local authority assessments can take 12 weeks or longer to complete. Understanding what happens when savings run out in a care home uk is the first step; the second is executing a logistical plan that protects the resident's stability. Use the Guide2Care directory to identify providers that maintain active contracts with your specific council. Our database includes over 17,000 registered care locations, allowing you to filter results by region and service type to ensure a seamless transition.

Establish a "Care Folder" immediately to keep the transition on track. This folder should contain the registered Lasting Power of Attorney (LPA) documents, the most recent financial assessment letter from the council, and the current residency contract. Having these documents ready prevents delays that could lead to fee arrears. It's also vital to consult a specialist financial adviser. Look for professionals accredited by the Society of Later Life Advisers (SOLLA). They provide specific calculations on whether a third-party top-up is sustainable or if financial products like an Immediate Needs Annuity could bridge a funding gap.

This experience often underscores the importance of robust long-term financial planning for the entire family. Understanding various investment strategies is a key part of building a secure future. For those exploring how to grow their capital, resources from investment specialists such as BGS Capital can provide valuable insights into different asset classes.

Quality remains a priority during any funding change. Always verify the latest Care Quality Commission (CQC) ratings on our provider pages before making decisions about a potential move. According to the CQC State of Care 2023 report, 81% of adult social care services were rated as good or outstanding. If a care home refuses to accept the local authority's set rate, you may need to find a new provider that meets these quality standards while staying within the state's budget. Our platform simplifies this search by providing direct links to the most recent inspection summaries for every listed home.

Finding the Right Care Provider

Use our advanced search filters to identify homes with specific specialisms, such as dementia or bariatric care. When you contact care managers, ask directly about their "council contract" policies. Specifically, ask what percentage of their current residents are state-funded. This data indicates how experienced the home is with local authority billing. Verify the latest CQC inspection reports via our provider pages to ensure that a lower price point doesn't result in a lower standard of clinical safety or resident dignity.

Final Checklist for Families

Confirm that the Lasting Power of Attorney for Property and Financial Affairs is registered with the Office of the Public Guardian. You must also notify the Department for Work and Pensions (DWP) of the funding change. Most disability benefits, such as Attendance Allowance or the care component of Personal Independence Payment (PIP), usually stop after 28 days of state-funded care. Ensure all parties are informed to avoid overpayment penalties. For more practical tools and provider listings, Find the care you need in our comprehensive directory.

Secure Your Future Care Funding

You'll need to notify your local authority at least 12 weeks before your capital hits the £23,250 threshold, or the specific limits set by the 2026 reforms. This timeframe allows the council to complete a fresh means test and ensure state funding starts exactly when your private funds finish. Understanding what happens when savings run out in a care home uk allows you to prepare for potential top-up fees or assessments for NHS Continuing Healthcare. Guide2Care offers clear, neutral guidance updated for the 2026 legislative changes to simplify these financial transitions. Our comprehensive directory lists thousands of CQC-registered providers, giving you the tools to find a home that fits your budget and care needs. Don't wait until funds are critical to start your search. Organise your strategy now to maintain continuity of care and protect your residency.

Find the care you need: Search our directory of UK care providers

Take control of your care journey today for a more secure and predictable tomorrow.

Frequently Asked Questions

Will the council take my parent’s entire pension to pay for care?

No, the council won't take your parent's entire pension to pay for care. They must leave the resident with a statutory Personal Expenses Allowance (PEA). In England, this amount is £30.15 per week for the 2024/25 financial year. The council uses the remaining pension income to offset the cost of the care home placement. This ensures your parent retains some money for their own personal use.

What is the "Personal Expenses Allowance" (PEA) in 2026?

The Personal Expenses Allowance for 2026 will be confirmed by the government in April of that year. It currently stands at £30.15 per week in England for 2024/25. This rate usually increases annually in line with inflation. Residents must be left with this specific amount after their pension income is applied to care costs. It ensures they can afford personal items like clothes, stationery, and snacks.

Can the care home evict my relative the day their savings hit the limit?

No, a care home cannot evict a resident the day their savings hit the limit. You must notify the local authority when capital falls below £23,250 to begin the funding transition. Understanding what happens when savings run out in a care home UK helps you manage this shift. The council will perform a financial assessment and, if eligible, they'll start paying the home directly at their agreed rate.

Do I have to sell my house if my spouse moves into a care home?

You don't have to sell your home if a spouse or partner still lives there. Under the Care Act 2014, the local authority must apply a statutory disregard to the property value in these circumstances. This rule also applies if a relative aged over 60 or a disabled relative lives in the house. Your home isn't counted as an asset during the financial assessment as long as they continue to reside there.

What happens if I cannot afford to pay a top-up fee for my parent?

The local authority must find an alternative care home that fits within their standard budget if you can't pay a top-up. If no suitable beds are available at the council's standard rate, the council must pay the higher fee themselves to meet the person's needs. You can't be forced to pay a top-up fee. Local authorities have a legal duty to provide at least one affordable option.

Is there a difference between "social care" and "nursing care" funding?

Yes, the funding streams differ because social care is means-tested while nursing care has a non-means-tested element. Social care covers daily living and is funded by the local authority. If a resident needs nursing care, the NHS pays a flat rate called NHS-funded Nursing Care (FNC). For 2024/25, the standard FNC rate in England is £235.88 per week. This is paid directly to the care home to cover nursing costs.

Can I give my savings to my children to avoid paying care fees?

No, you cannot give away savings to avoid paying care fees. This is classified as deprivation of assets by the local authority. They'll examine your financial history to see if capital was reduced intentionally to qualify for state funding. There's no time limit on how far back they can look. If the council identifies a deliberate gift, they'll assess you as if you still have that money in your possession.

How long does a local authority financial assessment usually take?

A local authority financial assessment usually takes between 4 and 6 weeks to complete. This process begins after the care needs assessment confirms that residential care is necessary. You should contact social services when savings drop toward the £23,250 threshold. They'll examine bank statements and property valuations to determine how much the council will contribute. Delays can happen if financial documentation is incomplete or missing during the application.