Downsizing for Retirement and Future Care: The Complete UK Guide (2026)

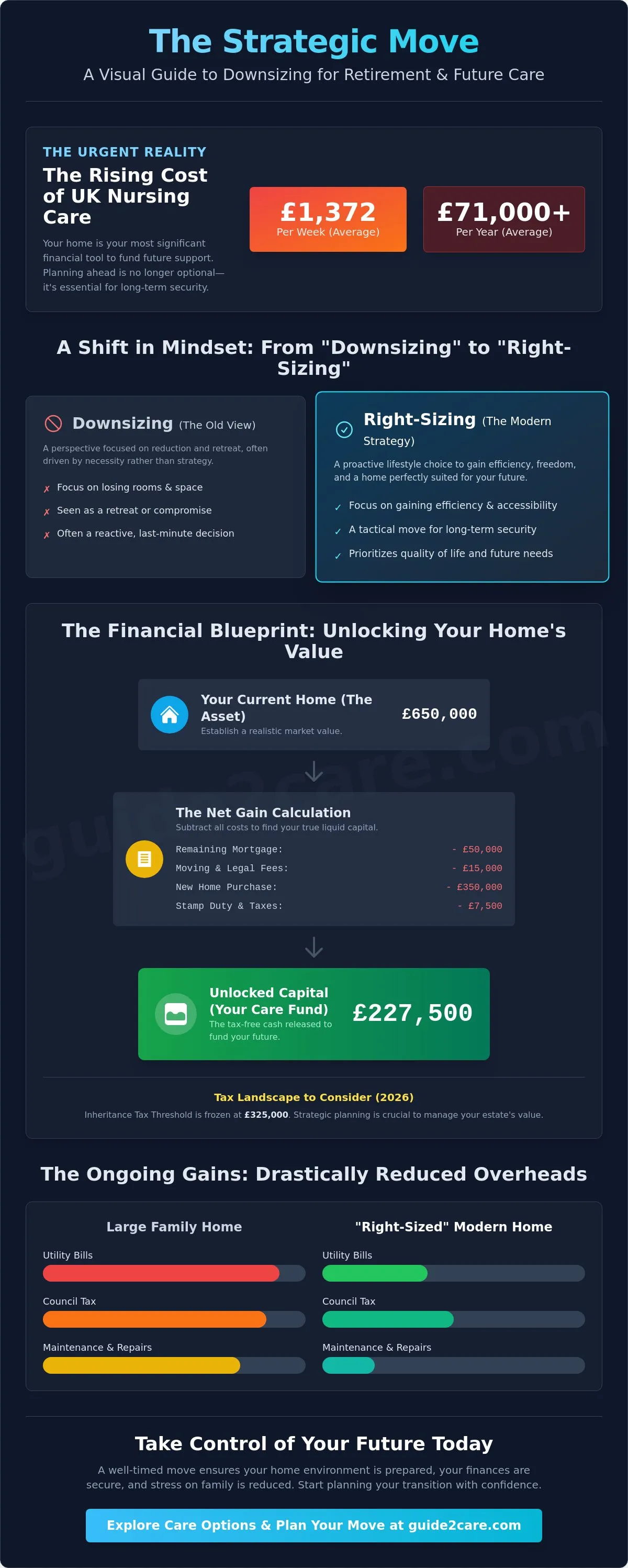

With UK nursing care costs now averaging £1,372 per week, your family home is no longer just a place of memories; it's your most significant financial tool. You likely feel overwhelmed by the relentless maintenance of a large property and anxious about how to fund support without exhausting your savings. Strategic downsizing for retirement and future care converts your property from an illiquid asset into a functional engine for your later life. It's time to stop viewing a smaller home as a retreat and start seeing it as a tactical move for long term security.

This guide shows you how to unlock equity and reduce overheads while future-proofing your lifestyle. We provide a clear breakdown of the 2026 tax landscape, including the frozen £325,000 inheritance tax threshold and current stamp duty rates. Follow our methodical approach to evaluate regional care costs and identify the right time to transition. Learn how to simplify your living arrangements and secure the funds necessary for high-quality care providers when you need them most.

Key Takeaways

- Redefine downsizing as a strategic "right-sizing" move to convert property wealth into liquid assets for future needs.

- Calculate your net financial gain by factoring in 2026 tax thresholds, stamp duty, and the true costs of downsizing for retirement and future care.

- Identify property features and locations that meet "Lifetime Homes" standards to ensure your next residence remains accessible as mobility changes.

- Follow a structured four-month decluttering timeline to manage the emotional and practical challenges of leaving a long-term family home.

- Use a care directory to audit local support services and understand the specific differences between home, residential, and nursing care options in your new area.

What is Downsizing for Retirement and Future Care?

Many homeowners compare this move to staying put or using equity release. Staying in a large family home often leads to escalating maintenance costs and expensive, reactive modifications. Equity release allows you to access cash but involves compounding interest that reduces the eventual value of your estate. In contrast, downsizing provides immediate capital without debt. Reviewing the history and types of UK housing for the elderly helps clarify how modern purpose-built properties differ from traditional residential houses.

To better understand how this transition functions as a financial strategy, watch this helpful video:

The Shift from Downsizing to Right-Sizing

Consider these benefits of a right-sized home:

- Lower monthly utility bills and council tax.

- Reduced time spent on property maintenance and gardening.

- Enhanced safety features like level thresholds and walk-in showers.

- Closer proximity to essential community services and transport links.

Why Future Care Must Be Part of the Conversation

Ignoring potential care needs during a move is a common mistake. UK nursing care costs currently average £1,372 per week; this equates to over £71,000 annually. Without liquid capital, funding this level of support becomes difficult. Your home should be an asset that facilitates care, not a barrier that prevents it. Large properties with stairs and narrow doorways often cannot accommodate mobility aids or live-in carers without significant structural changes.

Calculating the Financial Impact: Equity, Tax, and Running Costs

Calculating the net benefit of downsizing for retirement and future care requires a detailed analysis of transaction costs and tax implications. You must look beyond the headline sale price of your current home. Successful financial planning identifies the exact amount of liquid capital available after all liabilities are settled. This surplus forms the foundation of your long term care strategy. Start by obtaining three independent valuations to establish a realistic sale price. Subtract your remaining mortgage, if any, and estimated moving costs to find your true equity.

Reducing your monthly outgoings is a primary goal. Smaller properties typically incur lower Council Tax charges and significantly reduced heating bills. Modern apartments or bungalows often feature better insulation and more efficient heating systems than older family homes. These savings increase your disposable income, allowing you to contribute more to a dedicated care fund. You can search for local care providers to compare current service rates against your projected monthly budget.

Unlocking Property Wealth for Care Funding

Released equity creates a "care ringfence" to protect you from the high costs of professional support. In 2026, the average cost for nursing care in the UK is £1,372 per week. Having liquid assets ensures you can fund this independently if you exceed the £23,250 local authority funding threshold. Be aware of Inheritance Tax (IHT) rules. The nil-rate band remains frozen at £325,000 until 2028. The Residence Nil-Rate Band (RNRB) provides an additional £175,000 allowance. If you downsize to a less valuable home, you may still be eligible for "downsizing additions" to preserve your RNRB. Consult a qualified tax professional to confirm how these rules apply to your estate.

The Hidden Costs of Moving in the UK

Strategic Right-Sizing: How to Choose a Home That Supports Future Care

Compare different housing models before committing to a purchase. Standard residential bungalows or ground-floor flats offer the most independence but require you to manage all maintenance. Sheltered housing schemes provide a warden or scheme manager and communal areas for social interaction. Retirement villages often include extensive on-site amenities and emergency call systems. Each option has different implications for your lifestyle and future care options. Research the specific service charges and event fees associated with managed communities to avoid financial surprises later.

The Future-Proof Property Checklist

Use the "Lifetime Homes" standards as your benchmark for a care-ready property. These sixteen design criteria ensure a home remains usable as your needs evolve. Prioritize level access at all entry points to eliminate trip hazards. Wide doorways and hallways are essential for wheelchair or walker navigation. Check if the internal walls are strong enough to support grab rails or a hoist if required later.

- Wet Room Potential: Ensure the main bathroom can be converted into a walk-in shower area.

- Ground Floor Living: If buying a house, confirm there's a room that can serve as a bedroom near a downstairs toilet.

- Stairlift Compatibility: Measure the stairs to ensure they can accommodate a lift without blocking access for others.

- Low-Maintenance Exterior: Opt for smaller, paved, or raised-bed gardens to reduce physical labor.

Location and the "Care Ecosystem"

The location of your new home dictates the quality of your "care ecosystem." Proximity to a GP surgery and a pharmacy is a non-negotiable requirement for managing health in later life. Analyze the density of home care agencies in the new postcode. A high concentration of providers often leads to better availability and more competitive rates for domiciliary support.

Research the Care Quality Commission (CQC) ratings for care homes within a five-mile radius. Even if you plan to stay at home, living near an "Outstanding" or "Good" rated facility is a strategic advantage. It simplifies the transition if short-term respite or permanent nursing care becomes necessary. Don't overlook the importance of informal support. Position yourself near family or established social networks to ensure you have a reliable circle of help for daily tasks and emotional wellbeing.

Managing the Transition: From Emotional Hurdles to Practical Decluttering

Establish a clear communication plan with adult children early in the process. Involve them by asking which specific items they wish to inherit now rather than later. This reduces the volume of goods to be moved and ensures sentimental objects remain within the family. Use a structured approach to prevent conflict and ensure everyone understands the timeline. Clear decisions today prevent your children from facing a significant administrative and physical burden in the future.

Overcoming the Emotional Weight of the Family Home

The Practicalities of Decluttering for a Move

Execute a tactical four-month timeline to manage a large family home without exhaustion. Dedicate one month to each major area of the property. Start with low-emotion zones like the loft, garage, and garden shed. Use the "Keep, Sell, Donate, Bin" framework for every individual item. This methodical system prevents decision fatigue and ensures steady progress toward your moving date.

- Month 1: Clear out storage areas, lofts, and outbuildings.

- Month 2: Evaluate guest bedrooms and secondary living spaces.

- Month 3: Process the kitchen, bathrooms, and home office.

- Month 4: Finalize the main living areas and sentimental collections.

Integrating Your Move with Future Care Planning

Differentiate between the levels of support before you settle. Home care involves professional visits to your residence for daily tasks. Residential care provides a full-time living environment with support for personal needs. Nursing care includes 24-hour medical supervision by registered nurses. Establish a Lasting Power of Attorney (LPA) for both health and finances during the moving process. This legal step ensures trusted individuals can manage your affairs if your capacity changes in the future.

Mapping Local Care Services with Guide2Care

Use a specialized directory to identify the care ecosystem in your target area. Search for home care agencies that operate within your new neighborhood. Verify the Care Quality Commission (CQC) ratings for every provider to ensure they meet national standards for safety and effectiveness. You can use the directory to find care homes near me to understand the local capacity for higher-level support. This research prevents you from moving to a "care desert" where services are limited or oversubscribed.

The Final Step: Updating Your Care Plan

Complete the administrative transition to secure your long term benefits. Notify the Department for Work and Pensions (DWP) and your local council of your change of address immediately. Register with a new GP surgery and provide them with a summary of any existing care requirements or medical history. This ensures continuity of prescriptions and health monitoring.

- Update Your Will: Reflect your new property assets and any changes in your financial situation.

- Review Funding: Recalculate your care budget based on the final equity released from your sale.

- Inform Local Services: Check if your new local authority offers specific support schemes for older residents.

Finalize your plan by reviewing your care funding strategy. The scrapped social care reforms mean you remain responsible for your costs if your assets exceed £23,250. Use your new property value to confirm your ability to self-fund if your needs escalate. This methodical preparation ensures your move provides both a home and a secure financial future.

Secure Your Future Through Strategic Planning

Transitioning to a smaller home is more than a move; it's a structural change to your long term security. You've identified how to unlock equity and select a property that adapts to your physical needs. Successfully managing downsizing for retirement and future care requires a balance of financial precision and practical foresight. By addressing these factors now, you avoid the stress of reactive decision making during a health crisis. This proactive approach ensures your home remains a sanctuary rather than a source of maintenance or accessibility challenges.

Use our resources to finalize your transition. We provide a comprehensive directory of UK care homes and agencies alongside practical guides on care funding and selection. These tools help families make informed care choices and ensure the new location supports your long term health requirements. Find and compare UK care providers to future-proof your retirement. You're now equipped to build a lifestyle that prioritizes ease, accessibility, and financial independence. Start your search today to align your new home with the highest standards of professional support available in your area.

Frequently Asked Questions

Is downsizing for retirement always a good idea financially?

Downsizing is only financially beneficial if the difference in property prices significantly outweighs the transaction costs. High stamp duty, legal fees, and estate agent commissions can erode your expected profit. Calculate your net gain by subtracting all moving expenses from the anticipated equity release. It's often more about lifestyle ease and reducing maintenance than pure profit.

How does downsizing affect my eligibility for UK social care funding?

Releasing equity through downsizing for retirement and future care often increases your liquid capital above the £23,250 threshold. In England, if your total assets exceed this limit, you're responsible for the full cost of your care. Because the proposed care cap was scrapped, you'll likely remain a self-funder until your assets drop below this level. Having liquid cash allows you to choose your own providers instead of relying on state-funded options.

Can I downsize and still leave a significant inheritance to my children?

You can still leave a substantial inheritance by utilizing the downsizing addition for the Residence Nil-Rate Band. This rule allows you to pass on the full £175,000 allowance to direct descendants even if you move to a less valuable property. The main nil-rate band of £325,000 also remains available. This ensures that downsizing for retirement and future care doesn't automatically reduce the tax efficiency of your estate.

What is the best age to downsize for future care needs?

The best age to move is generally between 60 and 70. This window allows you to manage the physical demands of decluttering and packing while you're still active. Moving early ensures you're settled in an accessible environment before any mobility issues arise. It also gives you time to build a social network and establish links with local GPs in your new community.

Will downsizing affect my UK State Pension or other benefits?

Your State Pension remains unaffected by your property value or your savings. For the 2026/27 tax year, the full New State Pension is £241.30 per week. However, means-tested benefits like Pension Credit are impacted by the capital released from your home. If your total savings exceed £10,000, your eligibility for these specific benefit payments will decrease.

How do I find CQC ratings for care providers in my new area?

Should I sell my house and rent in retirement instead?

Renting offers flexibility but exposes you to rising costs and potential eviction. Owning a smaller property provides long term security and keeps your capital tied to an asset that can fund future nursing care. Consider renting only if you need to move quickly or aren't certain about a specific location. Most retirees find that home ownership offers more stability as their health needs change.

How much does it cost to move house when downsizing in the UK?

Budget for costs totaling approximately 3% to 5% of your property's sale price. Key expenses include estate agent fees of 1% to 1.5% plus VAT and legal fees for both the sale and purchase. You must also account for Stamp Duty Land Tax on the new property. In 2026, you'll pay 2% on the portion of the purchase price between £125,001 and £250,000.