Paying for Care Home Fees in the UK: 2026 Complete Funding Guide

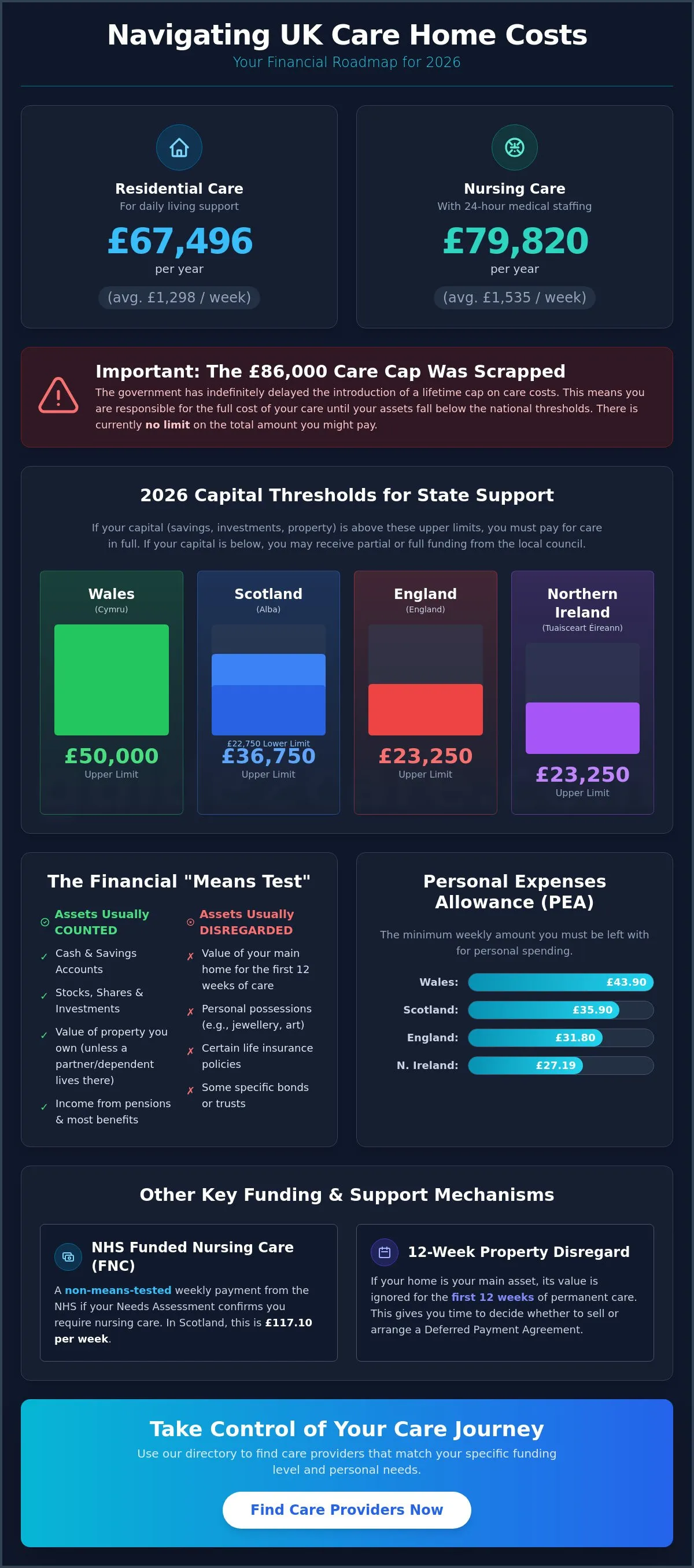

The average annual cost of residential care in the UK has reached £67,496. This figure often leaves families wondering how they will manage the cost of paying for care home fees uk without exhausting their life savings. You likely find the means test confusing and worry about the potential impact on your family home. It's a complex situation that requires clear, factual answers rather than vague advice.

This guide provides a practical roadmap through the 2026 funding system. You'll get the exact capital thresholds for England, Scotland, Wales, and Northern Ireland so you know precisely where you stand. We also explain which benefits are available to everyone, regardless of their financial status. Use this information to navigate the financial assessment with confidence and avoid hidden costs like top-up fees.

We'll start by defining the current capital limits and the step-by-step process for local authority assessments. From there, you can use our directory to find care providers that align with your specific funding bracket and care requirements.

Key Takeaways

- Identify the differences between residential and nursing care fees and understand the impact of the scrapped 2026 care cap.

- Learn how the financial assessment works when paying for care home fees uk, including which assets and savings the council will count.

- Compare state support rates with self-funding options to understand your level of choice and control over care providers.

- Discover how to use a Deferred Payment Agreement to fund care costs without the immediate need to sell the family home.

- Match your funding plan to a specific facility by using our directory to search for care providers by type and location.

Understanding Care Home Fees and the 2026 Landscape

Managing the cost of paying for care home fees uk requires a clear understanding of the 2026 regulatory environment. Many families expected the introduction of a lifetime care cap of £86,000, but the government scrapped these plans. This means you're responsible for the full cost of your care until your assets fall below specific thresholds. There's currently no limit on the total amount you might pay over several years, making early planning essential; as part of your long-term wealth strategy, you can check out BGS Capital to explore pre-IPO and IPO investment opportunities.

Fees split into two distinct parts. Personal care costs cover physical assistance and medical support, while "hotel" costs cover your accommodation, meals, and utilities. These combined expenses vary significantly across the UK due to local property markets and staffing availability. Currently, the average annual cost for residential care is £67,496, while nursing care reaches £79,820. These figures illustrate the financial pressure within Social care in England and the devolved nations.

To better understand how these costs are structured, watch this helpful video:

Before looking at providers, you must undergo a Needs Assessment. This professional evaluation determines the specific level of support you require. It's the essential first step that dictates whether you'll be looking for residential or nursing care. Once your needs are established, the local authority conducts a financial assessment to determine how much you'll contribute toward paying for care home fees uk.

Residential vs. Nursing Care Costs

Residential care averages £1,298 per week, focusing on daily living support. Nursing care is more expensive, averaging £1,535, due to 24-hour medical staffing. If a Needs Assessment confirms you require nursing support, you may receive NHS Funded Nursing Care (FNC). In Scotland, this is £117.10 per week and is not means-tested, providing a vital non-contributory payment for all eligible residents.

The 2026 Capital Thresholds

The 2026 thresholds trigger state support. In England and Northern Ireland, the upper limit is £23,250. Scotland's upper limit is £36,750, while Wales is £50,000. If your assets exceed these values, you'll pay the full cost. If they fall between the upper and lower limits, such as Scotland's £22,750 lower limit, the council provides partial funding based on a sliding scale assessment.

The Financial Assessment: How the "Means Test" Works

Once a Needs Assessment confirms you require care, the local authority conducts a financial assessment. This means test determines your exact contribution toward paying for care home fees uk. The council examines your total income, such as state and private pensions, alongside your capital assets. They'll ask for bank statements, investment records, and property valuations to build a complete financial profile.

Most forms of capital count toward the total. This includes cash in savings accounts, stocks, shares, and the value of any property you own. However, your home is excluded if a spouse, partner, or certain dependent relatives still live there. Some items are always ignored, such as personal possessions and certain life insurance policies. For a deeper look at specific exclusions, consult Age UK's guide to paying for a care home.

You aren't required to spend every penny on care. You retain a Personal Expenses Allowance (PEA) each week to cover small personal items like stationery or toiletries. In 2026, these mandatory rates are:

- England: £31.80

- Scotland: £35.90

- Wales: £43.90

- Northern Ireland: £27.19

Once you understand your budget, search our directory to find facilities that meet your financial requirements.

The 12-Week Property Disregard

If you own a home and your other assets are below the upper capital limit, the council ignores your property's value for the first 12 weeks of permanent care. This period gives you time to decide whether to sell the house or arrange a different payment method. It's a mandatory disregard that prevents immediate financial crisis when moving into a home. Eligibility usually depends on your other savings being below the threshold of £23,250 in England.

Deprivation of Assets: Rules to Avoid

Don't give away assets specifically to qualify for state funding. Local authorities call this "deliberate deprivation." There's no seven-year rule for care fees like there is for inheritance tax. Councils can look back indefinitely into your financial history. If they decide you gave away money or property to avoid paying for care home fees uk, they may assess you as if you still own that capital. Legitimate gifts are allowed, but the timing and intent are the critical factors the council will investigate.

Self-Funding vs. State Support: Comparing Your Options

Choosing between self-funding and state support significantly impacts your choice of care provider. Self-funders have the widest range of options. If you're paying for care home fees uk independently, you can select any facility that has a vacancy and meets your personal preferences. This path offers more control over room sizes, locations, and specific amenities. However, you're responsible for the full cost, which averages £1,298 per week for residential care across the UK.

State support is governed by the "Standard Rate." This is the maximum amount a local authority is willing to pay to meet your assessed needs. Councils often negotiate lower rates with providers than private individuals pay. If you rely on council funding, your choice is limited to homes that accept this standard rate. If you want a more expensive home, you must find a way to bridge the financial gap between the council's contribution and the home's actual price.

Self-funding carries the risk of capital depletion. If your assets fall toward the £23,250 threshold in England, you must contact the council for a reassessment. It's vital to do this early. The council might not agree to pay the home's private rate, which could lead to a request for a move to a cheaper facility. To avoid this, check if your chosen provider has a contract with the local authority before you move in. You can use our directory to identify providers that accept both private and local authority placements.

The Role of Third-Party Top-Ups

A top-up fee is the difference between the council's standard rate and the care home's fees. Usually, the resident cannot pay this themselves because the council assessment has already determined they can't afford more than the standard rate. A third party, such as a family member or a friend, must pay this fee. The third party signs a contract with the council and becomes legally responsible for the payments. They must demonstrate they can afford the cost for the duration of the resident's stay.

NHS Continuing Healthcare (CHC)

NHS Continuing Healthcare is a complete funding package for people with significant, ongoing health needs. It's not means-tested, so your savings and property aren't considered. If you qualify, the NHS pays 100% of your care home fees. The assessment process is rigorous. First, a healthcare professional completes a "Checklist" to see if you're eligible for a full evaluation. If you pass this stage, a multi-disciplinary team conducts a "Full Assessment" to determine if your primary need for care is health-related rather than social.

Strategic Ways to Fund Care Without Selling the Home

Many families worry that paying for care home fees uk requires an immediate house sale. This isn't always the case. You can use several financial tools to delay or avoid selling the family property while ensuring care costs are covered. These options allow you to retain the home's value for the future while meeting current financial obligations.

A Deferred Payment Agreement (DPA) is the most common method. It acts as a loan from your local authority. The council pays your care costs and secures the debt by placing a legal charge on your property at the Land Registry. This ensures the council can recover the funds at a later date without forcing an immediate sale during a stressful transition.

Deferred Payment Agreements (DPA) Explained

To qualify for a DPA, your property must be included in the financial assessment and your other assets must be below the upper capital limit. In England, this means your savings and investments must be less than £23,250. The council also checks that the property's value is sufficient to cover the long-term care costs and any accrued interest.

Local authorities charge interest on these loans to cover their costs. The government sets this rate, and it typically changes every six months. You will also face administrative fees for the setup and annual maintenance of the agreement. The loan usually becomes repayable 90 days after your death or as soon as the house is sold. This timeline provides your family with the necessary space to manage the estate without immediate financial pressure.

Non-Means-Tested Benefits: Attendance Allowance

You can use specific benefits to help with the cost of paying for care home fees uk. Attendance Allowance is available to individuals over State Pension age who have a physical or mental disability. Because it's not means-tested, your income and savings levels do not affect your eligibility. It's an essential source of extra income that you can apply directly to your care costs.

There are two weekly rates based on the level of care you need. The lower rate is for those needing help during either the day or the night. The higher rate is for those needing help during both. If you're a self-funder, you continue to receive this benefit while in a care home. However, if the local authority pays for your care, the benefit usually stops after you've been in the home for 28 days.

Another option to consider is an Immediate Needs Annuity. You pay a one-time lump sum to an insurance company in exchange for a guaranteed, tax-free income for life. This income is paid directly to the care provider, ensuring your fees are met regardless of how long you remain in care. Explore your options by looking for providers that work with different funding models. Browse our care home directory to find facilities that accept deferred payments and private funding.

Taking Action: Finding the Right Care Provider

After establishing your budget and understanding the 2026 thresholds, move to the practical search. Finding a provider that aligns with your specific funding model is crucial to avoid future relocation. Whether you are self-funding or relying on local authority support, your choice must match the provider's contractual terms. Choosing the wrong facility can lead to financial strain if the home does not accept council rates once your private funds deplete.

Use the Care Provider Directory to streamline your search. This platform allows you to filter results by location and specific care type, including nursing, residential, or dementia care. Categorizing your search this way ensures you only contact facilities equipped to handle your assessed needs. If you are paying for care home fees uk via local authority support, look specifically for providers that accept council standard rates. This prevents wasting time on facilities that require private premiums or third-party top-ups that your family may not be able to sustain long-term.

Using the Guide2Care Directory

Start your search by defining your geographical requirements and the level of care confirmed in your Needs Assessment. Our directory provides a structured way to compare different facilities side-by-side. You can filter for providers that offer specialized dementia units or those that provide nursing staff on-site 24 hours a day. Identifying these features early helps you build a shortlist of facilities that are both affordable and appropriate for your medical requirements.

Questions to Ask During a Care Home Visit

Visit your shortlisted homes in person. Financial transparency is just as important as the quality of care. Ask direct questions about their pricing structures to avoid hidden costs. Inquire about how often fees increase and the typical percentage of those increases. You should also ask if the home allows residents to stay if they transition from self-funding to local authority funding. Some homes require a minimum period of self-funding before they accept council rates.

Request a sample contract during your visit. Review the breakdown of room and board costs compared to personal care costs. Verify the notice period required for fee changes and the terms for any required deposits. This step protects you from unexpected expenses after the move. Ensure the contract clearly states the funding source and the protocol for when assets fall below the capital limits. A thorough contract check is the final step in securing a stable financial future while paying for care home fees uk.

Secure Your Financial Future in Care

Managing the costs of paying for care home fees uk requires a methodical approach to financial planning. You now understand how the 2026 capital thresholds trigger state support and how tools like a Deferred Payment Agreement can protect your property assets. Use these facts to choose a funding path that offers long-term stability. Early preparation ensures you remain in control of your care choices and avoids the stress of last-minute financial decisions.

The next stage is to identify a provider that matches your budget and care requirements. Our platform offers a comprehensive UK-wide directory with updated resources for 2026 care standards. We provide neutral and independent guidance to help you navigate this transition efficiently. Use our search tools to filter by location, care type, and funding acceptance to find the right fit for your situation.

Find and compare UK care homes on Guide2Care to begin your search today. You have the information needed to make a confident and informed decision about your future care.

Frequently Asked Questions

Do I have to sell my house to pay for care home fees in 2026?

You don't have to sell your house immediately to cover costs. The council ignores your property's value for the first 12 weeks of permanent care if your other assets are below the threshold. You can also apply for a Deferred Payment Agreement, which acts as a loan secured against your home. This allows you to delay paying for care home fees uk until the property is sold later.

What is the upper capital limit for care home funding in the UK?

The upper capital limit varies by region. In England and Northern Ireland, the limit is £23,250. In Scotland, it's £36,750, and in Wales, it's £50,000. If your savings and property value exceed these amounts, you're responsible for the full cost of your care. Once your assets fall below these figures, you become eligible for council support.

Can the council take my pension to pay for care?

The council includes most income, including state and private pensions, when calculating your contribution. You'll use this income to pay for your care, but you're legally entitled to keep a Personal Expenses Allowance. In England, this is £31.80 per week. In Wales, the allowance is higher at £43.90, ensuring you have money for personal items.

What happens if my money runs out while I am in a care home?

Notify your local authority as soon as your assets approach the upper capital limit. They'll perform a new financial assessment to determine your eligibility for state funding. It's vital to start this process early. If the home's fees are higher than the council's standard rate, you may need a third-party top-up to stay in the same facility.

Is Attendance Allowance means-tested if I move into care?

Attendance Allowance is not means-tested, so your income and capital don't affect your eligibility. If you're a self-funder paying for care home fees uk, you can continue to receive this benefit to help with costs. However, if the local authority contributes to your fees, the benefit usually stops after you've been in the home for 28 days.

How can I protect my inheritance from care home fees?

You cannot legally give away assets solely to avoid care costs. The council investigates "deliberate deprivation of assets" and can look back indefinitely at your financial history. Legitimate protection strategies include setting up specific trusts or changing property ownership to "tenants in common." Always seek specialist legal advice before making these changes to ensure they're compliant with current regulations.

What is the difference between social care and healthcare funding?

Social care covers daily living assistance and is means-tested based on your wealth. Healthcare funding, known as NHS Continuing Healthcare (CHC), is for individuals with a "primary health need." If you qualify for CHC, the NHS pays 100% of your care home fees regardless of your savings or property value. This is a health-based assessment rather than a financial one.

How much does the NHS contribute to nursing care home fees?

The NHS pays a flat weekly rate called NHS Funded Nursing Care (FNC) if you're assessed as needing nursing support. This payment is made directly to the care home to cover the cost of registered nursing staff. In Scotland, the FNC rate is £117.10 per week as of May 2026. This contribution is not means-tested and is available to both self-funders and state-funded residents.