Understanding the Care Cap in the UK: 2026 Funding Rules Explained

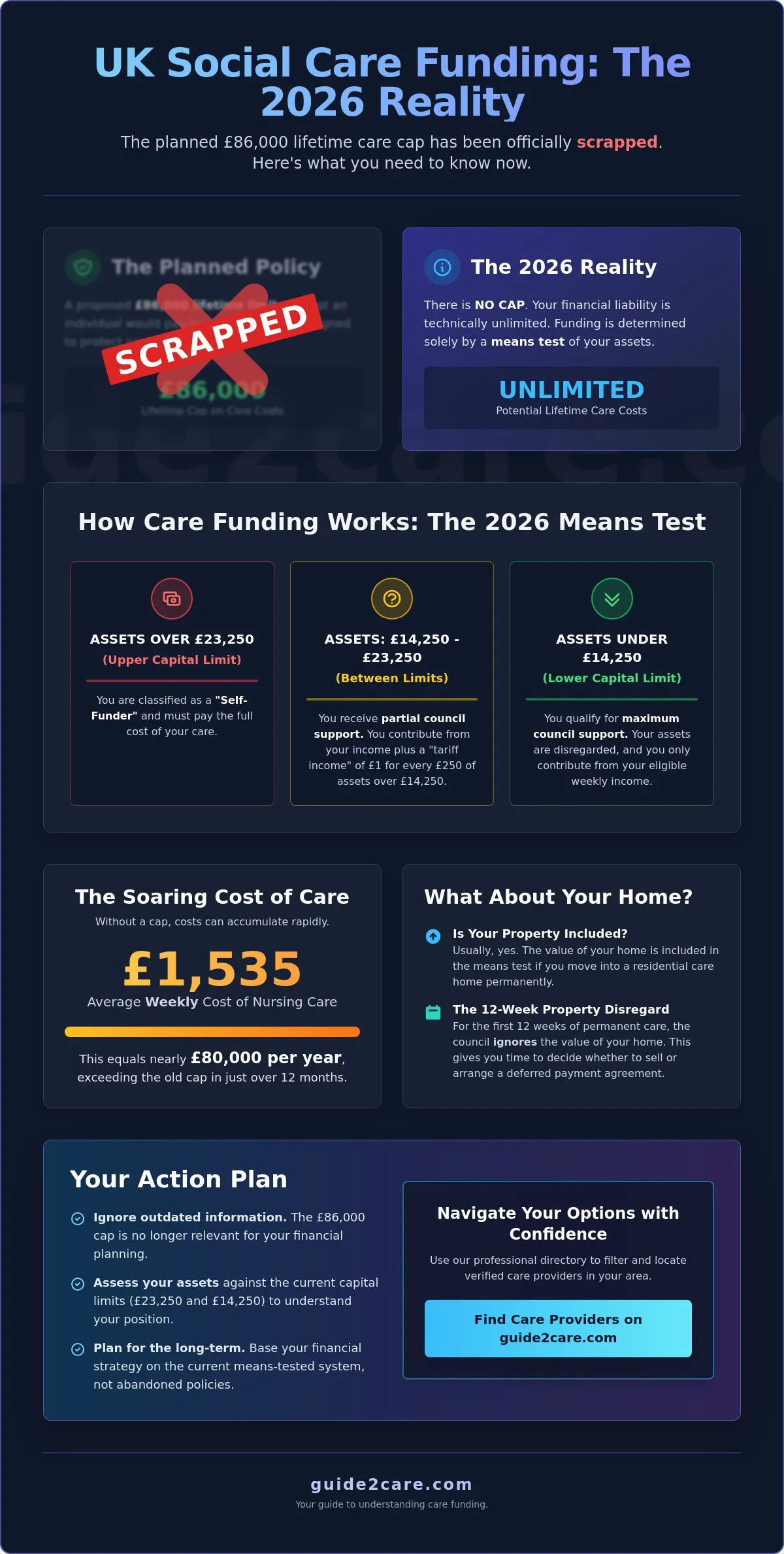

The planned £86,000 lifetime limit on social care costs has been officially scrapped. Many families anticipated a safety net for their savings, but understanding the care cap in the uk in 2026 requires a return to the traditional means-tested framework. If your assets currently exceed the upper capital limit of £23,250, you're responsible for the full cost of your care fees without a state-mandated ceiling on your total spending.

It's natural to feel frustrated by changing government policies and the complexity of local authority assessments. This article provides a clear, factual breakdown of the 2026 funding rules to help you plan with confidence. Review the specific financial thresholds for state support and the average weekly costs for residential services. Use this information to navigate the system and access our directory to find verified care providers in your area.

Key Takeaways

- Confirm the current status of the £86,000 lifetime limit and why it no longer applies to 2026 care planning.

- Improve your understanding the care cap in the uk by identifying the specific 2026 capital thresholds for state funding.

- Compare the differences between self-funding and local authority placements to determine your level of choice and control.

- Recognize the legal implications of asset deprivation and how to protect your property within government guidelines.

- Use our professional directory to filter and locate care providers based on specific service types and regional availability.

The UK Care Cap in 2026: Fact vs Fiction

The "care cap" refers to a proposed £86,000 limit on how much an individual would pay for personal care over their lifetime. This policy was designed to protect assets and prevent families from losing their homes to pay for long-term support. However, understanding the care cap in the uk in 2026 requires acknowledging that this limit is no longer government policy. The history of the social care cap involves years of legislative debate and multiple delays, leading to significant public confusion.

To better understand the core differences between social care and health care, watch this helpful video:

The reality for 2026 is that the cap has been officially abandoned. The current government scrapped the planned October 2025 implementation during the 2024 fiscal cycle. Confusion persists because the cap was postponed several times before its final cancellation. Many advice documents and news articles from previous years still refer to the cap as an upcoming reality. You must ignore these outdated sources. In 2026, self-funding remains the default for anyone with significant savings or property. You'll continue to pay for your care as long as your assets remain above the state thresholds.

The 2024/2025 Policy Shift Explained

The decision to jettison the charging reform framework occurred primarily due to budgetary constraints identified in late 2024. The 2024 Autumn Budget confirmed that the funding originally earmarked for the care cap would be redirected to other local government priorities. This shift effectively ended the transition toward a capped-cost model. Consequently, local authorities have stopped preparing the digital systems needed to monitor individual spending. For the 2026/2027 financial year, there is no lifetime cap on social care costs in England.

Why the £86,000 Figure is No Longer Relevant

The £86,000 figure is a policy ghost that no longer exists in any legal framework. It's important to differentiate between care types to understand why this matters. Even if the cap had launched, it wouldn't have covered "hotel costs" such as food and accommodation. Now, with the cap scrapped, your financial liability is technically unlimited. If you live in a care home for several years, your total spend could easily exceed £200,000 based on 2026 average nursing care rates of £1,535 per week. Plan your finances based on current means-testing rules rather than abandoned promises.

How Social Care Funding Works: The 2026 Means Test

The means test is the standard procedure used by local authorities to calculate your financial contribution toward social care. This assessment reviews your income, savings, and assets to decide if you qualify for state help. While previous discussions on understanding the care cap in the uk suggested a limit on total spending, the current system relies entirely on this means-tested approach. Your local council will look at your "liquid assets," such as cash in the bank, and your "fixed assets," which include property and land. Each authority follows national guidelines to ensure consistency, but they have some discretion over how they calculate certain disability-related expenses.

The Upper and Lower Capital Limits

The 2026-2027 financial year maintains specific thresholds for capital. If your total assets exceed the Upper Capital Limit (UCL) of £23,250, you're classified as a "self-funder" and must pay the full cost of your care. Once your assets fall below this amount, the local authority begins to contribute. The How Social Care Funding Works circular provides the full legal framework for these assessments. If your assets are between £14,250 and £23,250, the council applies "tariff income." This assumes you have £1 of weekly income for every £250 of savings you own. If your assets are below the Lower Capital Limit of £14,250, the council ignores them, and you only contribute from your weekly income.

How Your Property is Valued in 2026

Your home is usually included in the means test if you're moving into a residential care home. However, the 12-week property disregard rule applies when you first enter permanent care. During these first 12 weeks, the council ignores the value of your home to give you time to decide on a sale or a deferred payment agreement. Your property is also disregarded if a spouse, partner, or a relative who is over 60 or incapacitated still lives there. For those receiving care in their own home, the value of the property is generally excluded from the calculation. You can search our directory of local care providers to find services that match your specific funding situation.

Financial assessments for home care focus primarily on your disposable income. The council must ensure you keep a Minimum Income Guarantee (MIG) to cover daily living costs. For 2026-2027, this is £241.45 per week for individuals of pension credit age. Identify your specific MIG rate based on your age and disability status, as this dictates how much of your pension or benefits you can keep before the council asks for a contribution.

Self-Funding vs. Local Authority Support: A Practical Comparison

Choosing between self-funding and state support involves more than just a bank balance. Since there's no longer a limit on costs, The UK Care Cap: Fact vs Fiction research confirms that the financial burden rests heavily on the individual. Self-funders generally have total freedom to choose any care home that can meet their needs. Conversely, local authority placements are restricted to providers that accept the council's standard fee. Understanding the care cap in the uk means recognizing that these two paths have vastly different price points for the same level of service.

Research indicates that self-funder rates in 2026 are approximately 40% higher than the rates paid by local authorities for the same bed. For example, the average weekly residential care cost for a self-funder is £1,298, while nursing care averages £1,535. These higher private rates accelerate the depletion of your assets. Despite the cap's cancellation, the Care Act 2014 still places specific duties on local authorities. They must provide information and advice to all residents, regardless of their wealth, to help them make informed decisions about their long-term care.

The Rights of a Self-Funder

You have the right to a "Needs Assessment" from your council even if your assets exceed the £23,250 limit. This assessment identifies what support you require and helps you plan effectively. Local authorities must also provide brokerage services if you're unable to arrange care yourself, though some councils charge a fee for this. Monitor your savings closely. If your capital drops toward the £23,250 threshold, contact the council immediately. A transition to state funding isn't automatic and requires a new financial assessment to avoid a gap in care payments.

Local Authority Contracted Rates vs. Private Rates

Councils negotiate lower rates through block-buying contracts, a luxury private individuals don't have. If you choose a home that costs more than the council's "usual cost" limit, a third party must pay the difference. These are known as "top-up fees." You cannot usually pay your own top-up fee from your own capital unless you're in the 12-week property disregard period. Use this checklist to compare long-term costs:

- Ask the provider for their standard private rate and their local authority rate.

- Confirm if the home accepts residents at the council's rate if your funds run out.

- Identify if a family member is willing and able to pay a third-party top-up if required.

- Calculate total projected costs over five years, factoring in annual fee increases.

Planning for Care Costs: Strategies to Protect Your Assets

The cancellation of the £86,000 limit means you must take proactive steps to manage your long-term financial liability. Understanding the care cap in the uk involves accepting that you are responsible for your own funding strategy. Start your planning early to ensure you have the widest range of options for your future support. While the state provides a safety net once your assets drop below £23,250, you should identify ways to supplement your income before reaching that threshold. Claim all non-means-tested benefits available to you. Attendance Allowance is a key benefit for those over state pension age who require help with personal care. Since it isn't based on your savings or property, it provides a consistent contribution toward your weekly fees.

Be cautious regarding the "deprivation of assets" rules. Do not give away your home or large sums of cash solely to qualify for local authority funding. Local councils have the power to investigate these transfers. There is no fixed time limit for how far back a council can look. If they decide you intentionally reduced your wealth to avoid care costs, they will assess you as if you still own those assets. This can leave you with a funding gap that your family may have to fill. Instead of gifting property, search our directory for care providers to understand the current market rates in your preferred area and budget accordingly.

Understanding the Deferred Payment Agreement (DPA)

A Deferred Payment Agreement acts as a loan from your local council secured against your property. The council pays your care home fees, and the debt is repaid later, typically when your home is sold or after your death. This arrangement prevents the need for an immediate house sale during your lifetime. To be eligible, you must have assets (excluding your home) worth less than £23,250. Be aware that councils charge interest on these loans to cover their costs. In 2026, interest rates are reviewed every six months, and you'll likely pay administrative fees to set up the legal charge on your property.

Legal Ways to Manage Care Funding

Establish a Lasting Power of Attorney (LPA) for both financial and health affairs. This legal document ensures a trusted person can manage your funding and care choices if you lose mental capacity. Consider an Immediate Needs Annuity if you want to cap your own costs. You pay a one-off lump sum to an insurance company in exchange for a guaranteed income that pays for your care for life. While the "7-year rule" is a standard benchmark for Inheritance Tax, it does not apply to social care assessments. Councils can challenge any gift regardless of when it was made if they believe the motive was to avoid paying for care.

Finding Quality Care Providers with Guide2Care

Guide2Care functions as a central resource hub for families managing the 2026 care landscape. Since the government abandoned the lifetime cap, you must find providers that align with your specific financial and medical requirements. Our directory simplifies this search by organizing providers into clear, manageable categories. Filter results by care type, such as nursing, residential, or dementia care, to ensure the facility meets your clinical needs. Reviewing CQC ratings directly on provider profiles helps you prioritize quality and safety from the start of your search.

Contact several providers to compare their private fee structures. Because self-funders often pay higher rates, obtaining multiple quotes is a practical step to protect your remaining assets. Ask each provider about their policy on residents whose funds eventually fall below the £23,250 limit. Successfully understanding the care cap in the uk requires this level of due diligence to avoid unexpected financial pressure later. Use our platform to streamline this data collection and compare providers side by side.

How to Use the Guide2Care Directory

Start your search by entering a postcode or town into the directory search bar. Refine your results using the specialism filters to find homes experienced in specific conditions like Parkinson's or respite care. Each provider profile contains essential contact details, service descriptions, and links to inspection reports. If you prefer to stay independent, use the platform to locate domiciliary care agencies that provide support in your own home. This structured approach allows you to build a shortlist of viable options in minutes.

Next Steps: From Information to Action

Request a needs assessment from your local council immediately. Even if you plan to self-fund, this assessment provides a professional record of the support you require. Use your Guide2Care shortlist to book visits to at least three different homes. Seeing a facility in person is the only way to evaluate the atmosphere and staff interactions effectively. Find and compare care providers in your area today to secure the best possible support for your circumstances.

Secure Your Future Care Strategy

The 2026 funding landscape requires a clear, proactive strategy now that the lifetime limit has been officially scrapped. Focus on the verified capital thresholds of £23,250 and £14,250 to determine your eligibility for state support. Understanding the care cap in the uk means accepting that traditional means testing remains the only framework for local authority help. You must rely on accurate data and early financial planning to protect your assets and ensure a high standard of care for yourself or your loved ones.

Our platform brings order to this complex process by providing a comprehensive directory of UK-wide care homes and home care agencies. We include integrated CQC ratings on provider profiles to ensure you make an informed decision based on quality and safety. You can also utilize our free resources and guides to help your family navigate the legal and financial requirements of the current system. Use these tools to compare providers and identify the best fit for your specific needs and budget.

Search the Guide2Care Directory to find local care providers now. Taking these practical steps today ensures you remain in control of your care journey and your financial future.

Frequently Asked Questions

Is the £86,000 care cap happening in 2026?

No, the £86,000 care cap isn't happening in 2026. The government officially cancelled this policy in late 2024. This change is central to understanding the care cap in the uk because it means there's no longer a safety net for lifetime spending. You'll continue to pay for your support as long as your assets remain above the council's thresholds.

Will I have to sell my house to pay for care in England?

You don't have to sell your house immediately. You can apply for a Deferred Payment Agreement, which acts as a loan from the council secured against your property. Your home is also disregarded if a spouse, partner, or a relative over 60 lives there. Check with your local authority for their specific administrative fees and interest rates for these agreements.

What is the current capital limit for care funding in 2026?

For the 2026-2027 financial year, the upper capital limit is £23,250. If you have assets above this amount, you're a self-funder and must pay the full cost of your care. The lower capital limit is £14,250. If your assets fall below this, you only contribute from your income. Understanding the care cap in the uk requires knowing these specific figures to plan your finances accurately.

Does the care cap apply to home care or just care homes?

The care cap doesn't apply to any care services in 2026 because the policy was scrapped. Both home care and residential care follow the same means-tested rules. Your local authority will assess your income and capital to decide how much you contribute toward your support plan, regardless of whether you receive care in your own home or a facility.

What happens if my money runs out while I am in a care home?

Notify your local authority immediately if your capital drops toward £23,250. They will perform a new financial assessment to determine your eligibility for state help. Don't wait until your money is gone; the council needs time to process your application and arrange funding. This prevents a gap in payments to your care provider and ensures continuity of support.

Can I give my house to my children to avoid care fees?

Gifting your house can be classified as "deprivation of assets." Local authorities have the power to investigate any asset transfers made to avoid paying care fees. If they decide you intentionally reduced your wealth, they will assess you as if you still own the property. This could leave you with a significant funding gap that you are unable to cover.

Are there any benefits that help with care costs regardless of my savings?

Yes, Attendance Allowance and Personal Independence Payment (PIP) are available regardless of your savings. These benefits aren't means-tested and provide a weekly contribution toward your care costs. Claim these as soon as you meet the health criteria. They offer essential financial support for both self-funders and those receiving local authority help without affecting your capital limits.

What is the difference between social care and NHS continuing healthcare?

Social care handles personal care and is means-tested. NHS Continuing Healthcare (CHC) is for those with a "primary health need" and is fully funded by the NHS. Eligibility for CHC is based solely on your health requirements, not your finances. If you qualify for CHC, the NHS pays for your entire care package, including the full cost of care home fees.