Cost of Assisted Living in the UK: 2026 Fees and Funding Guide

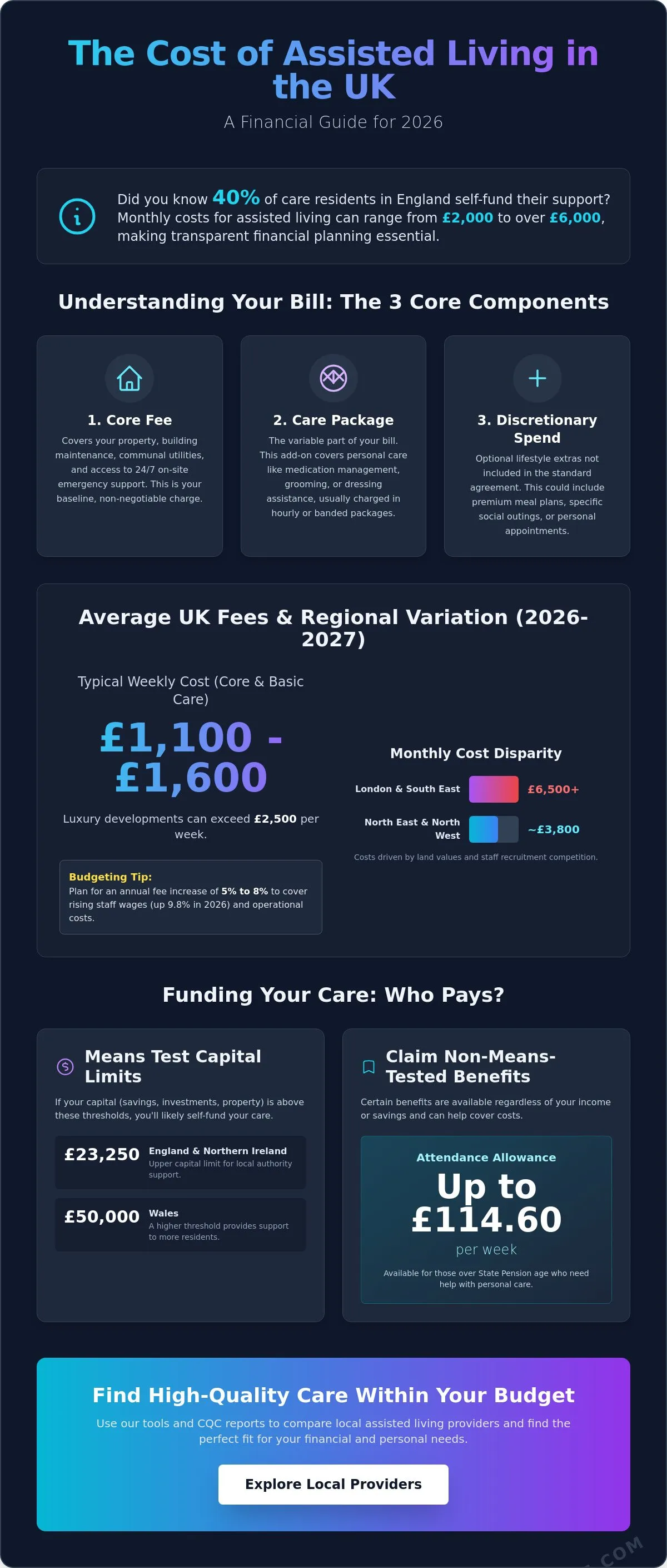

Did you know that 40% of care residents in England currently fund their own support, with the cost of assisted living uk now ranging from £2,000 to over £6,000 per month? It's difficult to plan for the future when service charges are unclear and the line between assisted living and residential care feels blurred. You likely worry about depleting your life savings or being surprised by hidden fees in 2026.

We understand that you need transparent figures to make an informed decision. This guide provides a comprehensive breakdown of 2026 fees, regional price variations, and the latest funding rules across the UK. Learn how the means test works, including the £23,250 capital limit in England and the £50,000 limit in Wales. Use this information to build a monthly budget and find the care you need by exploring local providers that fit your financial requirements.

Key Takeaways

- Identify the modular components of the cost of assisted living uk, including how core fees and personal care services combine into a total weekly budget.

- Compare the financial differences between assisted living, residential care, and live-in care to choose the most cost-effective model for 2026.

- Verify your eligibility for local authority support by understanding the 2026 capital limits, such as the £23,250 threshold in England and Northern Ireland.

- Discover how to claim non-means-tested benefits like Attendance Allowance, which provides up to £114.60 per week for those over State Pension age.

- Learn how to use directory tools and CQC reports to find and compare high-quality assisted living providers within your specific budget and region.

Understanding the Components of Assisted Living Costs

Understanding the cost of assisted living uk requires a breakdown of three specific modules. Unlike residential care, where you often pay a single flat fee for everything, assisted living in 2026 uses a modular financial structure. This means your total monthly bill is the sum of separate charges for housing, support services, and personal care. The Assisted living model separates these costs to give residents more control over their spending.

To better understand how these costs compare to other settings, watch this helpful video:

The three primary pillars of your budget include the Core Fee, the Care Package, and Discretionary Spend. The Core Fee acts as your baseline. It covers the right to occupy the property, building maintenance, and access to 24-hour emergency support. The Care Package is the variable portion of your bill. This includes help with medication management, laundry, or grooming. Finally, Discretionary Spend covers optional lifestyle choices. You might choose premium meal plans or specific social outings that aren't included in the standard service agreement.

Rent vs. Service Charges: What is Mandatory?

Service charges are almost always non-negotiable in purpose-built retirement blocks. These fees ensure the facility remains safe and operational. Typical inclusions cover building insurance, communal heating, and the presence of 24-hour on-site staffing. To manage these operational expenses effectively, many providers work with Green Compare for commercial utility procurement. Review your contract for "sinking fund" clauses. These are monthly contributions designed for long-term building maintenance, such as roof repairs or lift servicing. Sinking funds prevent residents from being hit with large, unexpected bills for major structural work. Identify these mandatory costs early to ensure your monthly budget is sustainable.

The Personal Care Add-on

Providers usually assess care needs through hourly rates or banded packages. This flexibility is a key benefit of the cost of assisted living uk model. It allows you to increase support as health needs change without the disruption of moving house. Personal care refers specifically to assistance with bodily functions like dressing, bathing, or eating, and it's a regulated activity under Care Quality Commission (CQC) standards. Most providers offer a review every six months to ensure you aren't paying for more care than you actually use. Compare different providers to see if they charge per 15-minute increment or use a minimum one-hour block.

Average Assisted Living Fees in the UK (2026 Data)

For the 2026-2027 financial year, the national average weekly cost of assisted living uk typically falls between £1,100 and £1,600. This range covers the core accommodation and a basic support package. Costs have trended upward following the 9.8% increase in staffing wages and general energy inflation recorded in early 2026, though many providers now use Green Compare to mitigate rising utility expenses. In major urban centers, luxury developments offering premium amenities such as on-site cinemas and fine dining often exceed £2,500 per week. These high-end facilities cater to those seeking a specific lifestyle alongside their care needs.

It is helpful to view these costs as a combination of rent and service charges. While the rent portion may stay stable, the service charge is more susceptible to annual inflation. This is because it covers the operational costs of the building and the wages of the on-site team. When you are planning your 2026 budget, you should allow for an annual fee increase of 5% to 8% to account for these rising operational expenses.

Regional Variations: London vs. The Rest of the UK

London and the South East remain the most expensive areas for care in the UK. Monthly fees in London often start at £6,500. By comparison, providers in the North East or North West may offer similar services starting around £3,800 per month. These variations stem from high land values and the increased cost of recruiting care staff in competitive urban markets. Many people refer to this model as Extra care housing, which provides a similar balance of independence and support. To see how these prices fluctuate in your specific area, you can search for local care providers to get direct quotes and compare regional data.

Hidden Costs to Budget For

Beyond the headline fee, several "hidden" costs require careful budgeting. Many assisted living contracts include a Deferred Management Fee (DMF), often called an exit fee. This is a percentage of the property value, sometimes reaching 10% to 30%, paid when the resident leaves or the property is sold. This fee covers the long-term capital costs of the development. In the institutional sector, these assets are often part of larger portfolios where investors explore Secondary Market Transactions to manage their strategic growth and liquidity. You should always ask for a clear breakdown of the DMF before signing a contract.

Additionally, confirm if your monthly service charge includes meals. Some providers offer a "pay-as-you-go" restaurant model, while others mandate a minimum meal spend of £200 to £400 per month. Finally, clarify how utility bills are handled. While communal heating is often covered in the service charge, individual electricity and water usage may be billed separately to your flat. For those needing to arrange their own home internet, broadbandfreedom.co.uk provides a platform to find fibre and connectivity options. Council tax is another significant expense. Most assisted living residents are responsible for their own Council Tax, though you may be eligible for a 25% single person discount if you live alone.

Comparing Assisted Living vs. Care Homes & Home Care

Choosing the right care setting requires a direct comparison of three distinct financial models. The cost of assisted living uk follows a modular structure where you pay for your housing and care separately. In contrast, residential care homes usually operate on an all-inclusive basis. This means one weekly fee covers your room, all meals, laundry, and 24-hour support. Home care uses an hourly model, which often seems cheaper initially but excludes the significant overheads of maintaining a private property.

Many individuals prefer staying in their current home to avoid moving costs. However, this choice involves hidden expenses that assisted living eliminates. You must still account for building insurance, emergency repairs, and rising council tax. To ensure your property remains fully protected during this transition, you can learn more about Just Quote Me for bespoke insurance solutions. When you add the cost of home care visits, which averaged £32.40 per hour in early 2026, the total monthly spend often exceeds the price of a purpose-built assisted living apartment. The value tipping point typically occurs when you require more than 20 hours of care per week.

For medical professionals who are weighing these property costs against future care needs, Mortgages for Doctors offers specialized mortgage and insurance advice to help manage housing assets effectively during this transition.

The Financial Case for Assisted Living

Assisted living offers specific financial advantages through its service structure. Personal care services are generally VAT-exempt when provided by a registered agency. This can make care-inclusive housing more tax-efficient than hiring private help for an unmanaged property. There is also a significant social value to these settings. Regular interaction and on-site support reduce isolation, which often prevents the decline in health that leads to expensive emergency hospital admissions. To evaluate your options, Find care homes near me and compare their all-in rates against the modular assisted living model.

When is a Care Home More Cost-Effective?

A care home becomes the more cost-effective choice when care needs become complex or constant. If you require 24/7 monitoring or specialized dementia support, the hourly cost of assisted living care will spiral. Residential homes benefit from economies of scale, providing 24-hour staffing at a lower per-person rate than individual home visits. The UK Government Care and Support Guidance outlines how local authorities must assess these needs fairly. For those with medical requirements, a Nursing Home vs Residential Care comparison can help you decide if the higher weekly fee of approximately £1,535 is necessary for your safety.

Funding Options: Who Pays for Assisted Living?

Securing financial support for the cost of assisted living uk involves a specific sequence of assessments. You should first request a Care Needs Assessment from your local authority. This meeting determines the level of support you require and whether your needs meet the national eligibility criteria. Once the council confirms you need care, you will undergo a Financial Assessment, also known as a means test. This process examines your income, savings, and assets to decide how much you must contribute toward your fees. If you are managing commercial assets or business interests as part of your financial portfolio, you can visit Green Compare to explore tailored finance solutions.

If your needs are primarily health-based rather than social, you may qualify for NHS Continuing Healthcare (CHC). This is a package of care arranged and funded solely by the NHS for individuals with significant and complex medical requirements. For those who own a property but lack liquid savings, a Deferred Payment Agreement (DPA) offers a solution. Under this arrangement, the local authority pays your care fees, and the debt is secured against your home to be repaid when the property is eventually sold. It is essential to ensure that such properties remain fully insured during this period, and Just Quote Me can provide the specialist insurance advice needed to protect your assets during this transition.

The 2026 Capital Limits and Self-Funding

The transition from self-funding to state support depends on strict capital thresholds. In England and Northern Ireland, the upper capital limit for the 2026-2027 financial year is £23,250. If your assets exceed this amount, you are responsible for the full cost of assisted living uk. In Scotland, the upper limit is higher at £35,000, while Wales maintains a single capital limit of £50,000 for residential care. When your savings fall below these thresholds, the local authority begins to contribute to your costs. If you choose a provider that charges more than the council's standard rate, your family may need to pay a "top-up fee" to cover the difference. If you are above these limits and looking for financial options to bridge any funding gaps, I Need Cash can help by matching you with personal or homeowner loan products tailored to your needs.

Benefits and Allowances to Claim

Several benefits can help offset your monthly expenses regardless of your savings. Attendance Allowance is a key resource for those over State Pension age who need help with personal care. For the 2026/27 period, the lower rate is £76.70 and the higher rate is £114.60 per week. Attendance Allowance is not means-tested, so your income and savings do not affect your eligibility. Younger residents may claim Personal Independence Payment (PIP) instead. Additionally, lower-income seniors should check their eligibility for Pension Credit, which can unlock further financial support and discounts on housing costs. You can explore our directory of care providers to find local options that accept local authority funding or top-up payments.

How to Find and Compare Assisted Living Providers

Finding a provider requires an organized approach to ensure the cost of assisted living uk aligns with the quality of service. Start by using the Guide2Care directory to filter options by location and care type. This tool allows you to narrow down hundreds of providers to a manageable shortlist in minutes. Once you have a list, examine the latest Care Quality Commission (CQC) reports for each facility. These documents provide independent ratings on safety and effectiveness, helping you determine if a provider's fee represents true value for money. A rating of "Outstanding" or "Good" is the standard you should look for to justify premium pricing.

During a facility tour, ask direct questions about historical fee increases. Request a written record of how much costs have risen over the last three years. In the care sector, the cheapest option is rarely the best. Lower fees often result from lower staffing ratios or reduced investment in facility maintenance. Focus on finding a balance between a sustainable budget and a high standard of care. To learn more about how efficient providers manage their background costs, you can discover Green Compare. High staff turnover, which often tracks with lower-priced facilities, can negatively impact the consistency of the care you receive.

Using the Guide2Care Directory for Price Transparency

Explore the "Funding Care" section on Guide2Care for localized guides. This resource provides specific data for different UK regions, helping you understand local price benchmarks. Look for "Premium Listings" on the platform; these providers often include detailed fee brochures and virtual tours to assist your decision-making. Always contact multiple providers to request a "Key Information Document." This standardized form makes it easier to compare the cost of assisted living uk across different organizations without getting lost in complex contracts. It clearly states what is included in the core price and what triggers additional charges.

Final Checklist Before Signing a Contract

Review the fine print for annual fee increase clauses before signing any agreement. Most providers link increases to the Retail Price Index (RPI) or Consumer Price Index (CPI) to account for inflation. Verify the notice period required to end the contract and check the refund policy for initial deposits. It's also vital to confirm what happens to your fee if you are hospitalized. Some providers offer a fee reduction of 10% to 20% if the room is unoccupied for more than a week, while others charge the full rate. Use these details to protect your financial interests. Find the care you need today with our comprehensive directory.

Plan Your Assisted Living Transition for 2026

Managing the cost of assisted living uk requires a clear understanding of modular fee structures and current funding thresholds. You now have the essential data to build a sustainable budget for the 2026-2027 financial year. For individuals who are also looking to grow their business assets to better fund these future needs, BGS Capital offers a strategic guide on how to find and connect with qualified investors in the UK. Remember that the capital limit in England is fixed at £23,250, and non-means-tested benefits like Attendance Allowance can provide up to £114.60 per week. These figures help you bridge the gap between self-funding and state support, ensuring you don't deplete your life savings unnecessarily.

The next step is to evaluate specific providers in your chosen region. Use our updated 2026 resources to compare service charges and care standards across the country. Our platform offers neutral, impartial guidance to simplify your search. You'll find comprehensive UK-wide listings that match your financial requirements and care needs. Our database reflects the latest 2026 care standards to ensure you find reliable providers. Take control of your care journey by using our tools today.

Find The Care You Need: Search Our UK Directory

Frequently Asked Questions

Is assisted living cheaper than a care home in the UK?

Assisted living is generally more cost-effective for individuals with low to moderate support needs. The average weekly cost of assisted living uk in 2026 ranges from £1,100 to £1,600, whereas residential care homes average £1,298 and nursing homes reach £1,535. However, if you require intensive 24-hour support, the modular hourly rates of assisted living can eventually exceed the all-inclusive fees of a residential home.

Will the council pay for my assisted living costs?

The local authority will contribute to your care costs if your capital falls below the 2026 thresholds, such as £23,250 in England or £35,000 in Scotland. Council funding typically only covers the personal care component of your bill. You're usually responsible for the rent and service charges—which are often managed more efficiently by providers who use Green Compare for utility procurement—though you may qualify for Housing Benefit or Pension Credit to help with these accommodation expenses.

Can I use my Attendance Allowance to pay for assisted living fees?

Yes, you can use Attendance Allowance to pay for any part of your assisted living fees. This benefit is paid directly to you and isn't means-tested, so your savings won't affect your eligibility. In the 2026/27 financial year, the higher rate provides £114.60 per week, which can significantly offset the cost of personal care packages or monthly service charges.

What are the hidden costs of assisted living I should look out for?

The most significant hidden cost is the Deferred Management Fee, or exit fee, which can reach 30% of the property's value when it's sold. You should also check for mandatory sinking fund contributions and separate billing for utilities like water and electricity. Some providers also charge extra for emergency call monitoring or administrative fees when you first move into the facility.

Do I have to sell my house to pay for assisted living in 2026?

You don't have to sell your home immediately if you use a Deferred Payment Agreement (DPA) with your local authority. This arrangement allows the council to pay your care fees and secure the debt against your property. The loan is only repaid when the house is sold later, providing a practical way to manage the cost of assisted living uk without a forced sale.

How much does the average service charge cost in a retirement village?

Service charges in UK retirement villages typically range from £500 to £1,500 per month in 2026. This fee covers mandatory services such as 24-hour emergency staffing, building insurance, and the maintenance of communal gardens and lounges. Facilities with premium amenities like swimming pools or on-site restaurants will naturally sit at the higher end of this price bracket. Operators of these facilities often use services like Green Compare to manage the significant utility costs associated with such amenities.

What happens if I run out of money while in assisted living?

You must request a new financial assessment from your local authority as your capital approaches the upper limit of £23,250 in England. Once your assets drop below this threshold, the council begins to contribute to your care costs. It's important to start this process at least 12 weeks before your funds reach the limit to avoid payment delays to your provider.

If you require temporary funding to cover care costs while waiting for your assessment to be processed, you can check out I Need Cash for help finding suitable loan options.

Is NHS Continuing Healthcare available for those in assisted living?

NHS Continuing Healthcare (CHC) is available to assisted living residents who are assessed as having a primary health need. If you're eligible, the NHS funds your entire care and support package directly. Unlike residential care settings, CHC in assisted living usually only covers the care elements, meaning you'll still need to fund your own rent, food, and utility bills.