The Ultimate Long Term Care Planning Checklist: A UK Guide for 2026

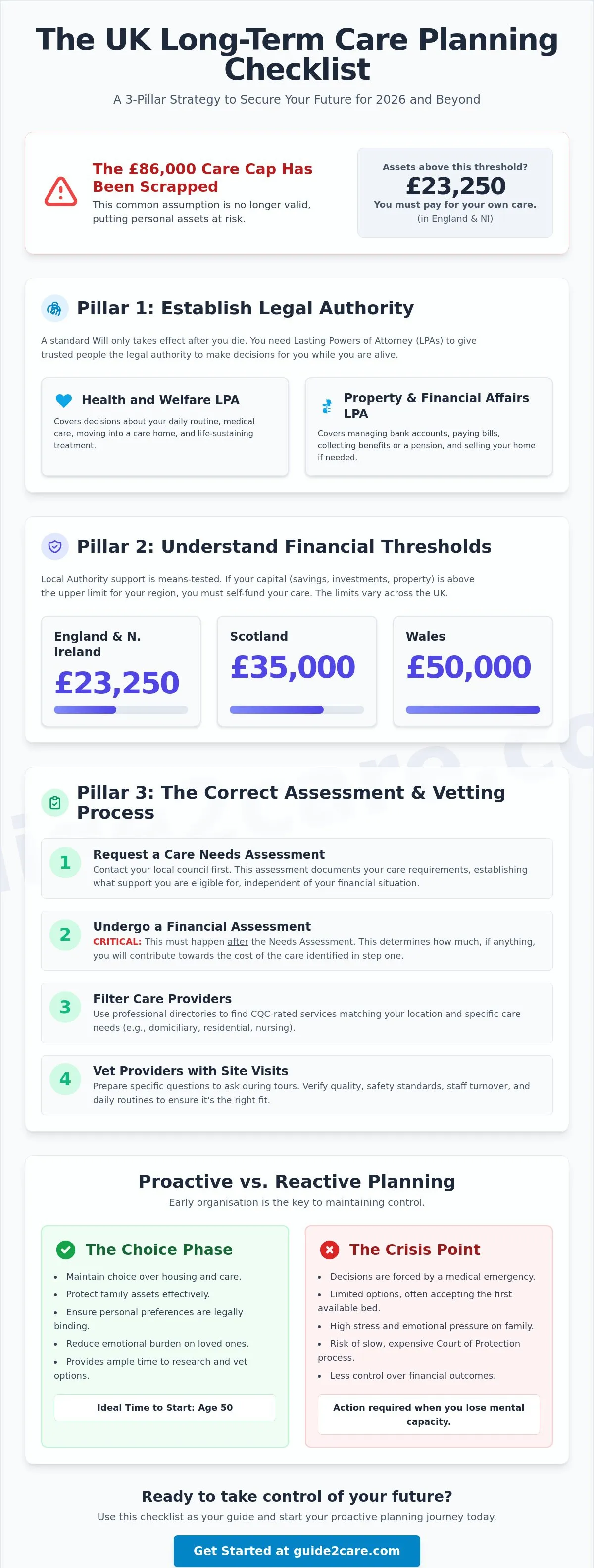

What if the assumption that the government will cover your care costs is the very thing that puts your family home at risk? With the proposed £86,000 care cap now officially scrapped, UK families face a system where assets above £23,250 in England and Northern Ireland mean you must pay for your own support. Organizing your future shouldn't happen during a medical crisis. Use this long term care planning checklist to build a three pillar strategy covering legal authority, financial protection, and quality care vetting.

You likely feel overwhelmed by the conflicting rules between NHS responsibilities and Local Authority means testing. It's common to worry about making rushed decisions that could impact your quality of life or your inheritance. This guide simplifies the process by providing a step by step framework to organize your affairs for 2026. You'll learn which legal documents are non negotiable, how to manage the current capital limits across the UK, and the most efficient way to evaluate care providers using professional directories. Follow these steps to secure your preferences and gain total peace of mind.

Key Takeaways

- Establish both Health and Welfare and Property and Financial Lasting Powers of Attorney. These documents provide legal authority that a standard Will cannot offer during your lifetime.

- Follow the correct sequence by requesting a Care Needs Assessment from your local council before undergoing a Financial Assessment. This ensures your care requirements are documented before your assets are means-tested.

- Use our structured long term care planning checklist to audit your current health and organize your financial records for 2026. Proactive preparation prevents forced, high-stress decisions during a health crisis.

- Filter care providers using professional directories to find services that match your specific location and care type. Learn which specific questions to ask during site visits to verify quality and safety standards.

- Transition from reactive to proactive planning to maintain choice over your housing and support options. Early organization is the most effective way to protect your preferences and financial security.

Why Start Your Long Term Care Planning Today?

Long term care planning is a proactive strategy to manage your health, housing, and financial security as you age. It is not a single document like a Will. Instead, it is a comprehensive roadmap for how you want to live when you can no longer perform daily tasks independently. Understanding What is Long-Term Care? helps define the services you might eventually require, ranging from domiciliary support in your own home to 24 hour residential nursing facilities.

Many UK families wait until a health crisis, such as a fall or a sudden illness, to consider these options. This delay leads to a "crisis point" where choices are limited. You might be forced to accept the first available care home bed, regardless of its quality or location. Planning ahead keeps you in the "choice" phase. It allows you to vet providers and secure your preferred living arrangements before an emergency removes your ability to decide.

To better understand the core components of this process, watch this helpful overview:

The Care Act 2014 remains the primary legislation governing how local authorities in England assess and meet care needs. It guarantees your right to a needs assessment, but it doesn't guarantee free care. A common misconception is that the NHS pays for all social care. The NHS only covers clinical medical needs through Continuing Healthcare (CHC) funding, which is notoriously difficult to secure. Most social care is means-tested. If your assets exceed £23,250 in England or Northern Ireland, you'll likely pay the full cost. Using a long term care planning checklist helps you identify these financial thresholds before they become a problem.

The Benefits of Early Organisation

Starting early ensures your personal care preferences are legally binding. Without a Lasting Power of Attorney, your family might need to apply to the Court of Protection to make decisions for you. This is a slow, expensive, and stressful process. Early organisation also allows for clear financial planning. Since the £86,000 care cap has been scrapped, understanding your local capital limits is the only way to protect family assets. By using a secure digital hub like SafeKeep to store your plans, you'll reduce the emotional burden on your loved ones by providing them with a clear set of instructions to follow during a medical emergency.

When is the Right Time to Plan?

The most effective time to start planning is before a need becomes urgent. While this guide focuses on senior care, proactive health monitoring is a lifelong commitment that often begins at the very start of a family's journey. For instance, many parents-to-be in the East Midlands choose a private pregnancy scan Mansfield to establish a foundation of professional care and clinical insight from the earliest stages of life.

The Legal and Financial Foundations of UK Care

A standard Will is insufficient for managing your affairs while you're still alive but require support. Your long term care planning checklist must prioritize legal tools that grant authority to trusted individuals during your lifetime. The UK legal framework relies on specific documents to ensure your health and financial preferences are honored if you lose mental capacity. Relying on family members to make informal decisions is risky; without legal standing, they may be unable to access your bank accounts or speak with medical professionals on your behalf.

The NHS care and support planning framework emphasizes that high quality care must be personalized to the individual. Legal documents like the Lasting Power of Attorney (LPA) and Advance Decisions provide the foundation for this personalization. These tools ensure that your voice remains central to the care process, even if you can no longer communicate your wishes directly.

Essential Legal Documents

You must register two types of Lasting Power of Attorney: Health and Welfare, and Property and Financial Affairs. Each requires a separate application to the Office of the Public Guardian and involves a registration fee. An Advance Decision to Refuse Treatment (ADRT) is also vital. This legally binding document specifies which medical treatments you do not want to receive in the future. Ensure your Will is updated to reflect these arrangements, as it remains the primary tool for asset distribution after death.

Financial Preparation and Funding

The UK care system is primarily means-tested. For the 2026 to 2027 financial year, the upper capital limit in England and Northern Ireland is £23,250. If your assets exceed this, you're responsible for the full cost of your care. Individuals in Scotland face a £35,000 threshold, while the limit in Wales is £50,000. For medical professionals concerned about how these limits affect their long-term security, Mortgages for Doctors provides expert advice on income protection and property management. If you have a primary health need, you might qualify for NHS Continuing Healthcare (CHC), which covers the full cost of care regardless of your wealth. However, eligibility is strictly assessed based on the complexity and intensity of your condition.

Given the strict nature of these capital limits, many individuals look to grow their private wealth through strategic investments to ensure they can afford their preferred care options. To learn more about how to access exclusive market entries, you can explore Investor Introduction and discover how BGS Capital connects qualified investors with pre-IPO and IPO opportunities.

If you own a home but lack liquid cash, a Deferred Payment Agreement (DPA) allows you to use the value of your property to pay care fees without selling it immediately. The local authority pays your costs and reclaims the money later. Once your legal and financial foundations are set, you can begin searching for care providers that align with your budget and location. This structured approach prevents the need for rushed financial decisions during a health crisis.

Evaluating Care Needs and Quality Standards

Establishing legal and financial foundations is only half the battle. You must evaluate the specific level of support required to ensure your daily needs are met safely. A long term care planning checklist is incomplete without a professional clinical evaluation. This process determines whether you require domiciliary care in your own home, residential care in a facility, or specialized nursing care for complex medical conditions. Each level of support carries different cost implications and regulatory requirements; for those on the business side of the sector, healthcarebizadvisors.com provides a strategic guide on hospice agency valuation methods.

The Local Authority Gatekeepers

Contact your local council's adult social services department to request a Care Needs Assessment. This is a legal right under the Care Act 2014, regardless of your financial situation. A social worker or occupational therapist will visit to evaluate your ability to perform activities of daily living, such as washing, dressing, and preparing meals. If you're eligible for support, the council will then conduct a Financial Assessment to determine who pays for the services. If you qualify for funding, you can choose "Direct Payments." This option gives you the cash to arrange and pay for your own care services directly, providing greater control over your daily routine.

Vetting Care Providers with CQC

Use the Care Quality Commission (CQC) website as your primary vetting tool for providers in England. The CQC inspects services and issues four ratings: Outstanding, Good, Requires Improvement, or Inadequate. Look beyond the overall rating and read the full report to understand the provider's specific strengths and weaknesses. Focus on the five key questions the CQC asks: Is the service safe? Is it effective? Is it caring? Is it responsive? Is it well-led?

A "Requires Improvement" rating shouldn't always lead to immediate dismissal. Check the date of the last inspection and see if the provider has addressed the specific failings mentioned in the report. However, if the "Safe" or "Well-led" categories are flagged as failing, consider it a significant risk. Integrating these quality checks into your long term care planning checklist ensures you select a provider that maintains high standards of dignity and safety. Domiciliary care allows you to stay at home with scheduled visits, while residential care provides a room and assistance with personal care. Nursing care is necessary if you have a medical condition requiring a registered nurse on site 24 hours a day. Distinguishing between these options early prevents you from paying for a higher level of care than you actually require.

The Ultimate Long Term Care Planning Checklist for 2026

This long term care planning checklist converts complex regulations into a series of actionable steps. Use this framework to move from theoretical preparation to practical execution. By following a chronological order, you ensure that legal authorities are active before they are needed and that your home environment remains safe as your mobility changes.

- Step 1: Audit your health. Review your current medical records and identify conditions that may require specialized support later. If you are considering private medical support for these assessments, you can find out more about accessible clinical services that help you decide between standard residential care or specialized nursing facilities.

- Step 2: Register your Lasting Power of Attorney. Submit your completed forms to the Office of the Public Guardian immediately. The registration process often takes up to 20 weeks, so you must act before a health crisis occurs.

- Step 3: Build an "Essential Information" folder. Compile a physical or secure digital file. Include your NHS number, GP contact details, a list of current prescriptions, and National Insurance numbers.

- Step 4: Perform a home safety audit. Evaluate your living space for "ageing in place" modifications. Check for trip hazards, assess the need for bathroom grab rails, and ensure your heating is reliable; for residents in the South West Scotland area, a professional boiler installation Moffat ensures your home stays warm and safe throughout the year.

- Step 5: Visit at least three providers. Physical tours are the only way to gauge staff engagement and facility cleanliness. Use our directory to search for care providers in your specific postcode to begin your shortlist.

Immediate Actions (The Next 30 Days)

Draft your LPA documents and formally notify the "people to be told" as required by UK law. This transparency prevents legal challenges later. Review your existing life or health insurance policies to see if they include long term care riders or cash value options. Additionally, catalog your digital assets and use a platform like SafeKeep to organize your digital estate. Record the locations of passwords for online banking, utility accounts, and social media. Share this access with your financial attorney to ensure they can manage your bills without delay.

Long-Term Research (The Next 6 Months)

Map the local care market by comparing home care agency hourly rates against residential care weekly fees. This data allows you to build a realistic budget based on the 2026 capital limits. Consult a SOLLA-accredited (Society of Later Life Advisers) professional. These specialists understand care funding products and can help you structure assets within the current legal framework. For qualified investors looking to grow their wealth to meet these future costs, BGS Capital provides access to specialized pre-IPO and IPO investment opportunities. Finally, hold a formal family meeting. Clearly document your end-of-life preferences and care goals to ensure your relatives are aligned with your wishes. This prevents conflict and ensures your plan is executed exactly as you intended.

Implementing Your Plan: Finding and Vetting Providers

Finalising your long term care planning checklist requires moving from administrative preparation to active provider selection. This stage involves filtering available services and conducting rigorous physical inspections. You must ensure the service provider can meet the specific clinical and social needs identified during your previous assessments. Whether you are considering a home care package from a provider like NeeryVille Care or moving into a care setting, you must verify that the provider's operational standards align with your expectations for safety and dignity.

Using the Guide2Care Directory

Use the Guide2Care directory to simplify the identification process. Filter your search by specific service types, including nursing care, residential care, or domiciliary home care. This targeted approach allows you to compare multiple providers within your specific UK postcode. Look for premium listings that offer detailed facility insights, such as staff specialisms and available amenities. Identify at least five providers that meet your basic criteria before scheduling any site visits or interviews. This structured comparison prevents you from settling for the most convenient option rather than the highest quality one. Additionally, for sourcing home aids and daily essentials, Anglia Market offers a way to support small and medium-sized businesses while finding the tools you need for independent living.

Questions for Your First Visit

Conduct thorough interviews with managers before signing any service agreements. Ask direct questions about their operational standards and staff management. Use these specific queries to gauge the quality of the environment:

- What is your staff-to-resident ratio during night shifts?

- How do you handle specific medical needs, such as dementia care or complex mobility requirements?

- Can I see your most recent CQC inspection report and the subsequent action plan for any flagged improvements?

- How do you integrate technology, such as digital social care records, into your daily routine?

Trial Periods and Quality Monitoring

Request a trial period in any residential care contract. Standard practice often includes a four week trial phase. This period allows you to evaluate the quality of care and social integration without a long term financial commitment. If the setting does not meet your needs, the trial period provides a clear exit strategy. Once a service begins, monitor quality consistently. Review the care records regularly and observe interactions between staff and residents. Check that the personalised care plan is being followed exactly as agreed. If you notice a decline in responsiveness or hygiene, reference the provider's CQC action plan immediately. Active monitoring is the final, ongoing step in your long term care planning checklist to ensure your safety and well being remain the priority.

Secure Your Future with Proactive Planning

Organizing your later life requirements doesn't have to be a reactive process driven by a health crisis. By establishing your legal authority through LPAs and understanding the 2026 capital limits, you maintain control over both your care and your assets. This long term care planning checklist provides the organizational structure needed to move from initial confusion to a finalized, actionable strategy. You now possess the tools to evaluate clinical needs and vet providers based on objective quality standards rather than convenience.

The final step is identifying a service that aligns with your specific location and support requirements. Use our comprehensive UK-wide directory to access CQC-integrated data and free resources designed for families. Start your search for the right care provider on Guide2Care today to ensure your preferences are documented and respected. Taking these practical steps now provides the long term security and clarity that you and your family deserve. You've built the framework; now it's time to implement the plan.

Frequently Asked Questions

What is the difference between an Advance Decision and a Power of Attorney?

An Advance Decision is a legally binding document that specifies medical treatments you wish to refuse in the future. It only covers health decisions and takes effect when you lose capacity. In contrast, a Lasting Power of Attorney (LPA) appoints a specific person to make decisions on your behalf. An LPA can cover both health and financial matters, providing broader authority than an Advance Decision alone.

Does the UK government pay for long term care?

The UK government only pays for social care if your assets fall below specific means-tested thresholds. In England and Northern Ireland, you must pay the full cost if your capital exceeds £23,250. The NHS pays for clinical care through Continuing Healthcare (CHC) funding, but this is only for individuals with complex, primary health needs. Most residents contribute significantly to their own support costs.

Will I have to sell my house to pay for care in 2026?

You don't always have to sell your home immediately to fund residential support. If a spouse, partner, or qualifying dependent still lives in the property, the council disregards its value during the means test. If the house is included in the assessment, you can apply for a Deferred Payment Agreement. This allows the local authority to pay your fees and reclaim the debt from your estate later.

How do I get a free Care Needs Assessment in the UK?

Contact the adult social services department of your local council to request a free assessment. This is a statutory right under the Care Act 2014 and is available regardless of your financial situation. A social worker will evaluate your daily challenges and document the support required. Completing this step is a vital part of your long term care planning checklist before you undergo a financial means test.

What is the "cap on care costs" and does it apply to me?

The proposed £86,000 cap on personal care costs has been officially scrapped by the government. It doesn't apply to anyone in the UK for the 2026 to 2027 financial year. Currently, there's no lifetime limit on the amount you might have to spend on your care. You're responsible for all costs until your assets drop below the upper capital limits defined by your local authority.

Can I choose my own care home if the council is paying?

You can choose your own care home if the facility meets your assessed needs and the council's budget. If you prefer a home that costs more than the local authority's standard rate, a third party can pay the difference. This is known as a "top-up fee." You cannot usually pay this fee yourself using your own restricted capital; it must typically come from a family member or friend.

What happens if I lose mental capacity before making a plan?

Your family must apply to the Court of Protection to become a "deputy" if you lose capacity without an LPA in place. This process is significantly more expensive and time-consuming than registering a Power of Attorney. Deputies have similar powers to attorneys but face stricter reporting requirements and annual fees. It's much more efficient to finalize your long term care planning checklist while you're still healthy and capable.

How often should I update my long term care checklist?

Review your care plan at least once a year or whenever your health or financial status changes significantly. Legislation and capital limits often update with the new financial year in April. Regular reviews ensure your documents reflect current UK regulations and your personal preferences. Keeping your records current prevents confusion for your family during a sudden medical emergency.